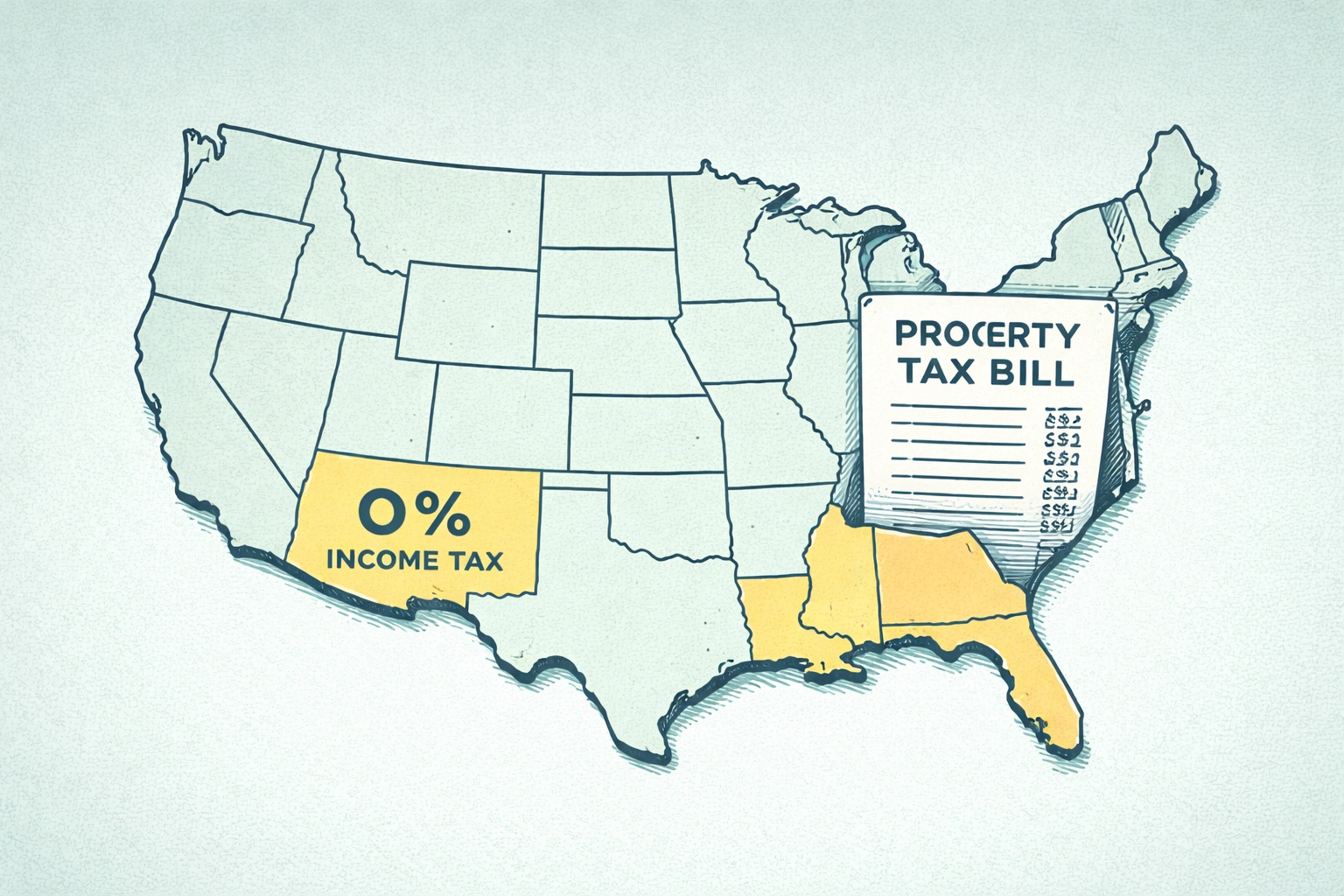

The pitch sounds airtight. California taxes your income at 13.3%. Texas taxes it at zero. Move from Los Angeles to Austin and you’ve given yourself an automatic 13-point raise without changing a single thing about your job or your skills.

I’ve watched a version of this calculation drive relocation decisions for people I know, and almost none of them ran the second half of the math before signing a lease.

Here’s what they missed: Texas doesn’t have an income tax because it’s generous. It has one because it funds state government through property taxes instead. The statewide average property tax rate in Texas runs around 1.6% — but in the metros where people actually want to live, it’s higher. Austin’s Travis County frequently hits 2.18%. Dallas-Fort Worth suburbs, particularly in newer developments built through Municipal Utility Districts, can exceed 2.5%.

Buy an $800,000 house in Austin and your annual property tax bill runs roughly $17,440. Buy that same $800,000 house in California — where Proposition 13 caps assessment increases — and your bill might be $5,680. That $11,760 annual difference consumes a significant portion of the income tax savings you relocated for.

And that’s before accounting for the cost of living shifts that don’t show up in any tax bracket. Texas has no public transit infrastructure in most metros, which means two-car households are effectively mandatory in a way they aren’t in New York or Chicago. Utility costs run higher. Austin’s housing market, after years of tech-driven migration, now has median home prices that rival parts of the Northeast — which means the affordability premium that justified the move a decade ago has partially eroded.

None of this means relocating is wrong. For the right income level, the right target city, and the right housing situation, moving to a lower-tax state produces real, lasting financial benefit. The problem is making that decision on incomplete information — optimizing for the headline rate while the silent costs quietly absorb what you saved.

The calculator below runs the full picture: federal and state income tax at your actual salary, property tax estimates based on state averages, sales tax drag, and cost of living adjustment by state. It doesn’t give you a recommendation — it gives you the number you should have had before the conversation started.

*Includes federal income tax (2025 brackets), state income tax (effective rates), and cost of living adjustment (MERIC/C2ER). Property tax and sales tax vary by city — see notes below your result.

How to Read Your Result

The output is your Real Buying Power — what your salary actually translates to in disposable purchasing capacity after the full tax picture and local cost of living are accounted for.

A few things worth knowing as you interpret it.

The property tax estimates use state averages, which in high-property-tax states like Texas can meaningfully understate what you’d actually pay in a specific metro. If you’re seriously evaluating Austin, Dallas, or Houston, look up the specific county rate and run it against the purchase price you’re considering — the difference from the state average can be several thousand dollars annually.

The cost of living adjustment uses the MERIC/C2ER index, which captures housing, transportation, utilities, groceries, and healthcare in aggregate. It’s a composite, so it won’t perfectly reflect any single city — Manhattan and upstate New York have the same state but wildly different living costs. For a more precise read on a specific city, NerdWallet’s cost of living calculator and BestPlaces let you compare at the city level.

The federal tax calculation uses 2025 brackets and assumes W-2 income. If your income includes capital gains, self-employment income, or RSU vesting — RSU taxation creates some specific state-level considerations worth understanding separately — the actual number will differ.

The Scenarios That Surprise People Most

A few patterns show up consistently when people run this honestly.

The California renter vs. Texas homeowner. Someone renting in a California city, who would need to buy in Texas to replicate their living situation, often finds the property tax differential and home price appreciation in Texas metros narrows the gap considerably. California’s Prop 13 creates anomalous long-term homeowner benefits that don’t show up in headline rate comparisons — people who bought in California fifteen years ago are paying property tax rates that would be impossible to replicate as a new buyer anywhere.

The remote worker arbitrage. The scenario where relocation works most cleanly: someone earning a coastal salary through remote work who moves to a genuinely lower cost-of-living market — not Austin or Miami, which have largely repriced to absorb the migration premium, but Raleigh, Columbus, Salt Lake City, or similar second-tier metros. The income stays constant, the cost base drops materially, and the tax differential is a genuine bonus rather than a wash.

The high earner in a high-income-tax state. At $400,000 in California, the income tax math becomes harder to dismiss. California’s top rate applies above $1 million but the 9.3% bracket starts at $61,000 for single filers, and the difference in take-home between California and a zero-income-tax state at that income level is real money. The wealth-building case for relocation gets stronger as income rises, because the absolute dollar value of the tax differential scales up while property tax exposure is capped by what you choose to spend on housing.

The Question Worth Asking Before You Run the Numbers

The financial calculation is the easy part. The harder question is what you’re optimizing for beyond the number.

Salary negotiation research consistently shows that geographic concentration in major metros correlates with higher compensation, better career optionality, and faster income growth — particularly early in a career. A lower-cost city can produce a higher Real Buying Power on your current salary while quietly limiting the ceiling of what that salary becomes over the next ten years.

The income vs. investment returns question applies here in a specific way: if a geographic move reduces your income trajectory — by removing you from the professional networks and opportunities concentrated in major markets — the tax and cost of living savings may not compensate for the compounding effect of slower income growth over a decade.

For people mid-career with established professional networks that travel with them, or for people working fully remotely with location-independent compensation, that concern matters less. For people early in their career in fields where physical proximity to opportunity still matters — finance, media, certain tech roles, law — the relocation math should include a realistic projection of what your income looks like in each location five years out, not just what it looks like today.

Run the full calculator. The one that includes the income trajectory, not just the tax rate on the cover page.