A friend of mine moved from Hyderabad to San Francisco for a job paying $115,000 a year. He called me three months in, genuinely confused. “I’m making more money than I ever have,” he said, “and I feel poorer than I did in India.” He wasn’t being dramatic. After rent, taxes, and basic expenses, he was saving less than $400 a month.

That conversation stuck with me. Because the number on his offer letter was real. The purchasing power it implied was not.

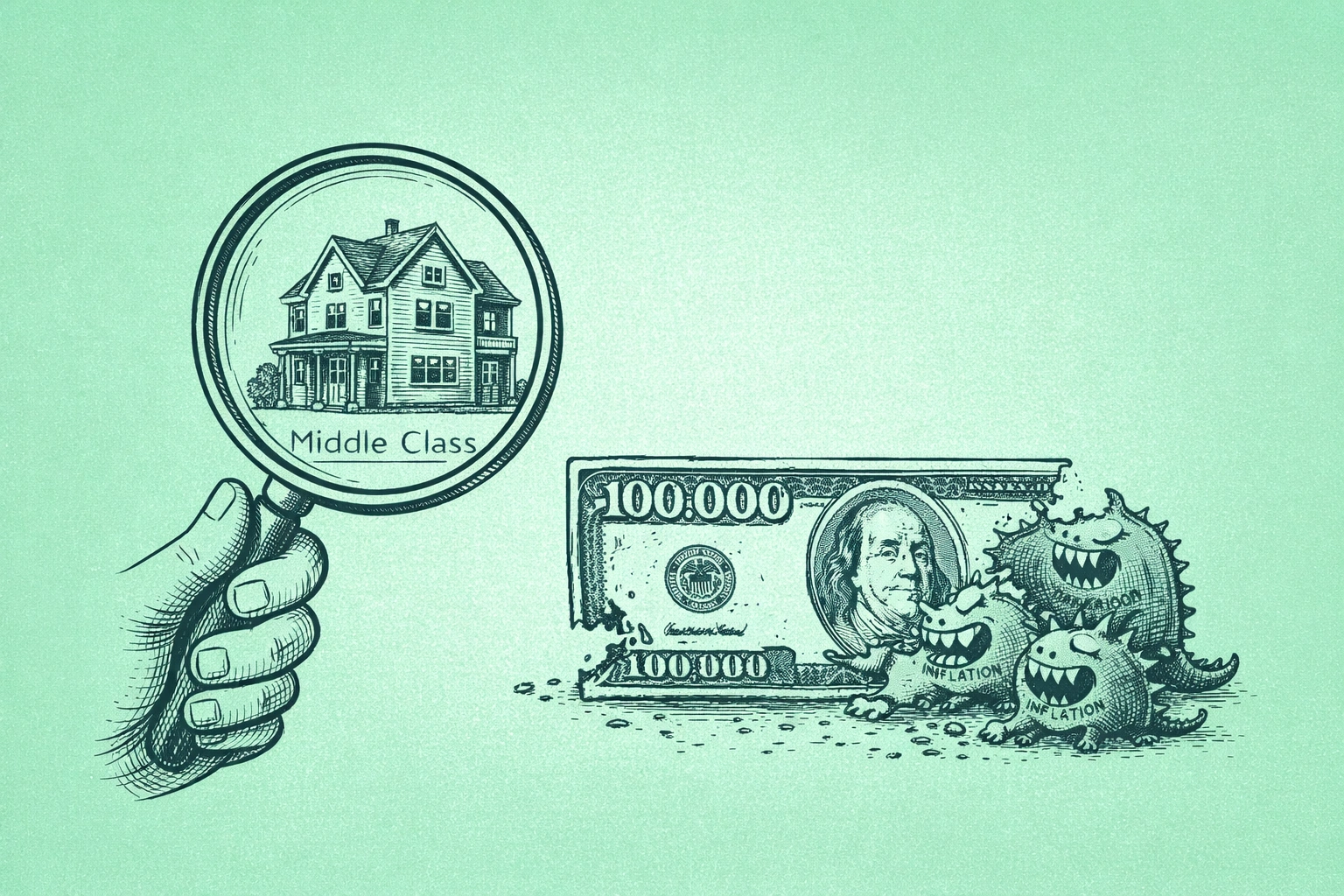

The median US household income hit $83,730 in 2024. That sounds solid. But a household earning $100,000 today has roughly the same purchasing power as one earning $80,000 had in 2020. Cumulative inflation from January 2020 through December 2024 ran approximately 25-30%, which means the number went up but the life it buys didn’t keep pace. Not even close.

The word “middle class” has become almost meaningless as an income descriptor. What it actually describes — the lifestyle, the security, the ability to own a home and save for retirement and send a kid to college without drowning — has quietly become something that costs significantly more than most people realize. Here’s what the real math looks like in 2026.

The Middle Class Income Range Is Wider Than You Think

Pew Research defines middle class as earning between two-thirds and double the median household income. Nationally, for a three-person household, that comes out to roughly $56,600 to $169,800.

That’s a wide band. But the number that really changes things is the geographic adjustment.

The income threshold to enter the middle class in Massachusetts is around $66,565. That’s higher than the median household income in fifteen other states. A household making $100,000 in Mississippi is comfortably upper-middle class — they can own a home, save, and probably take a real vacation. That same $100,000 in San Francisco means renting a one-bedroom and watching the retirement account grow at a rate that doesn’t feel like enough.

Same income. Completely different economic reality. And yet most people still benchmark themselves against the national median like geography doesn’t exist.

Why the Lifestyle Feels Broken Even When the Income Looks Fine

I’ve been tracking the actual cost of what most people think of as a middle-class life — not the vague concept, but the specific line items — and the numbers are genuinely alarming when you put them together.

Start with housing. The median home price nationally sits around $420,000. With a 20% down payment and a 7% mortgage rate, you’re looking at roughly $2,794 per month before property taxes or insurance. To keep housing costs below the recommended 28% of gross income, you need a household income around $120,000. That’s just to qualify for a median-priced home. In high-cost metros, the number climbs past $200,000 before the math makes sense.

Join The Global Frame

Money, work, and tech — one read every Saturday that actually changes how you think.

Then healthcare. The average family premium in 2024 ran $23,968 per year. Most employers cover a portion of that, but out-of-pocket costs — deductibles, copays, prescriptions — still add $5,000 to $10,000 annually for a typical family. This is not a luxury. It’s just not getting sick.

Then retirement. Fidelity recommends saving 15% of income to retire at a reasonable age. On a $100,000 income, that’s $15,000 a year. The actual median American savings rate is closer to 3.5%. The gap between those two numbers is where retirement insecurity lives.

College savings. One child at a four-year public university currently costs around $27,000 per year in-state. To fund that without loans, you need to save roughly $600 to $1,200 per month from birth. Most families aren’t anywhere near that number.

Add food, transportation, utilities, and any kind of emergency fund, and you’re looking at $88,000 to $100,000 per year before anyone buys a piece of clothing or takes a day off. The lifestyle that felt automatic to a previous generation now requires an income that puts you in the upper tier of earners.

The Part Nobody Talks About: Skills Required Just to Get Here

Something I noticed when I started reading the labor market data more carefully is how much the skill threshold has shifted, not just the income threshold.

In the 1980s, a mid-skill job — a trade, a clerical role, a basic administrative position — reliably produced a middle-income outcome. The OECD found that almost half of middle-income workers today are in high-skill occupations, compared to one-third two decades ago. You need more education and more specialized capability to land in the same relative economic position your parents occupied.

A bachelor’s degree in 2026 produces what a high school diploma plus a few years of experience produced in the 1990s — a starting point around $55,000 to $75,000, which in most cities puts you at the lower edge of middle class, not comfortably within it. The skills-based hiring shift that’s reshaping employment is partly a response to this: employers are increasingly less interested in credentials per se and more interested in whether you can do work that commands a premium. That’s a reasonable evolution, but it places more responsibility on workers to constantly evaluate whether their skills are keeping pace with the market.

This is also why salary negotiation has become a more urgent skill than it used to be. When the gap between market rate and your current compensation can represent the difference between building savings and running in place, leaving money on the table at the negotiation stage is expensive in a way it wasn’t when raises tracked inflation more reliably.

The Four Things That Actually Determine Your Class Now

Income is one input. It’s not the whole equation.

The first is location-adjusted purchasing power. Brookings found that in cities like San Francisco and New York, fewer than 52% of middle-class households can afford basic necessities. In more affordable metros — Dayton, Ohio, or Raleigh, North Carolina — that number climbs above 77%. Remote work has made this more negotiable than it used to be. Earning a coastal salary while living in a market where housing costs 60% less is one of the most direct paths to rebuilding the purchasing power the last five years eroded.

The second is debt load. The OECD’s research on middle-class financial vulnerability is stark: the middle class is increasingly over-indebted. Average student loan balances around $37,000, car loans around $24,000, credit card balances around $6,500. Someone earning $90,000 and servicing $67,000 in non-mortgage debt is not financially middle class regardless of the income number. They’re leveraged working class with a decent paycheck.

The third is equity accumulation. The wealth gap between income tiers is more revealing than the income gap. Median net worth for upper-income households runs around $805,400. For middle-income households it’s $106,100. You can earn $120,000 and still be building no wealth if the income disappears into housing costs and debt service. Someone earning $70,000 with a paid-off house in a stable market and a funded HSA and 401(k) is wealthier in any meaningful sense than the person with a better salary and nothing to show for it.

The fourth is career flexibility. The old middle class was defined by stability — one employer, thirty years, a pension. The new version is defined by adaptability. Skills that transfer across employers and industries, the ability to negotiate your own market value, some hedge against the risk that your current role gets restructured or automated. That’s not pessimism — it’s the realistic shape of the labor market in 2026, and building toward it is different from assuming tenure equals security.

What to Actually Do With This

The first move is honest geographic benchmarking. If you’re in a high-cost metro and the math genuinely doesn’t work — and you’ve run the actual numbers, not the approximate ones — remote work or relocation deserves a real evaluation rather than a vague intention. $95,000 in Raleigh and $180,000 in San Francisco often produce similar disposable income after housing and taxes. One of those numbers sounds twice as good. The actual life it funds isn’t.

The second move is shifting focus from income to net worth. Income is taxed heavily. Equity compounds. The tax-advantaged accounts — HSA first for families at $8,550 annually, then 401(k) match, then Roth IRA — save 20 to 35 cents on every dollar compared to taxable investing. That’s not a marginal improvement. Over twenty years, it’s the difference between having assets and having memories of having earned money.

The third is being ruthless about lifestyle inflation. A raise feels like permission to upgrade something — the apartment, the car, the travel. Sometimes that’s fine. But the compounding math on investing half of every raise is so favorable over a long period that it’s worth at least being deliberate about the decision rather than just letting lifestyle expand to fill available income.

The Honest Answer to Why $100K Feels Like $60K

Because in a lot of places, adjusted for what it costs to actually build a middle-class life, it essentially is.

The number hasn’t changed. What’s changed is that housing, healthcare, education, and retirement together now cost something that a previous generation didn’t have to fully fund at once — employer pensions covered retirement, college cost a fraction of what it does now, and housing in most markets was within reach on a single income.

My friend in SF eventually did the math properly and relocated. He’s earning $30,000 less in Austin. He’s saving $2,000 a month. He told me it was the best financial decision he’s made.

The income wasn’t the problem. The geography was making the income meaningless. Middle class in 2026 isn’t a number on a pay stub. It’s a set of conditions — ownership, savings, security, flexibility — and whether you’ve structured your financial life to actually build toward them.