2022 is the year the argument against the traditional balanced portfolio stopped being theoretical.

The S&P 500 fell roughly 18% that year. In a functioning 60/40 world, that should have been partially offset by the bond allocation — bonds are supposed to go up, or at least hold steady, when equities fall. It’s the foundational premise of the strategy. Stocks and bonds move in opposite directions, so holding both smooths out the ride.

Instead, long-term Treasury bonds fell over 30%. Corporate bond funds did similarly. Investors in “balanced” portfolios didn’t get cushioning — they got hit from both sides simultaneously. There was no hedge. The seesaw that the entire strategy depended on broke.

The reason isn’t complicated. When inflation spikes, central banks raise interest rates. Higher rates compress stock valuations by making future cash flows worth less in present-day terms. And higher rates crush existing bond prices directly — when new bonds are issued at higher yields, the older lower-yield bonds become less valuable. In an inflationary environment, stocks and bonds don’t move in opposite directions. They fall together.

This isn’t a new critique. Nassim Taleb has been making it for years. What 2022 did was provide a live demonstration that was hard to argue with.

What the Strategy Actually Is

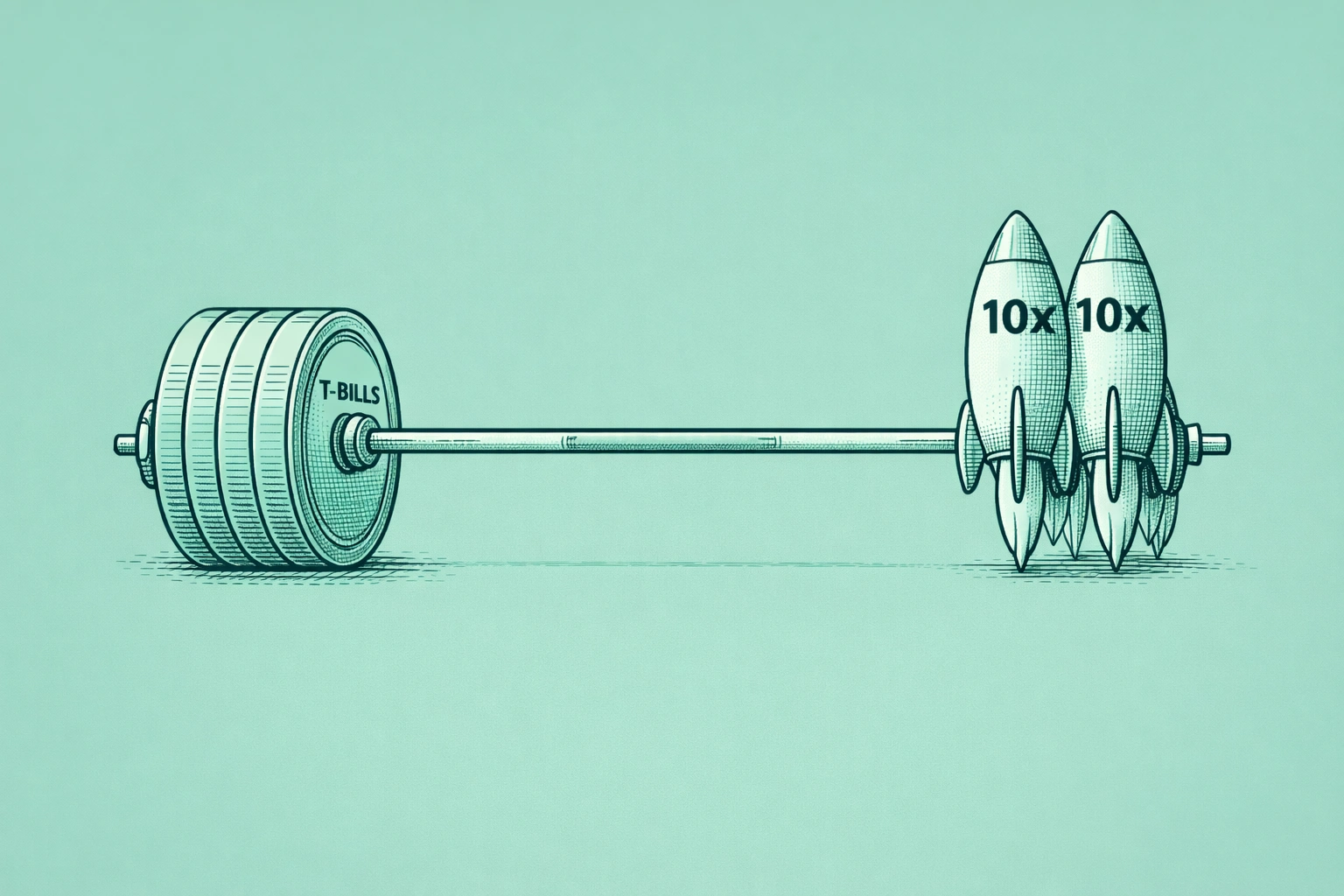

The barbell is a simple idea. Instead of positioning everything in the “safe middle” of moderate risk and moderate return, you go to both extremes deliberately — the vast majority of capital in genuinely safe assets, a small portion in genuinely high-risk, high-upside positions, and as little as possible in the middle.

The intuition behind it is about asymmetry. A conventional portfolio that’s 60% stocks and 40% bonds gives you roughly symmetrical risk. You can lose 20-30% in a bad year, and you can gain 10-15% in a good one. The ratio of potential loss to potential gain is roughly 1:1 or worse when you factor in inflation.

The barbell inverts that ratio on the aggressive side. If 10% of your portfolio is in genuinely asymmetric positions — things that can return 10x or 50x — then a complete loss of that 10% hurts but doesn’t define your financial life. But if one of those positions works, it doesn’t add 15% to your net worth. It changes the number entirely.

I’ve been thinking about this framing more seriously since 2022 validated the concern about bonds and since the index fund concentration question has gotten harder to dismiss. The middle ground feels safe because it’s familiar and because it worked for a long time. It doesn’t feel risky. That’s part of what makes it dangerous in an environment that’s structurally different from the one it was designed for.

The Safe Side: What Actually Belongs Here

About 90% of capital in a barbell structure goes to what I’d call the fortress — assets whose job isn’t to grow dramatically but to survive anything. The standard for this side isn’t “low risk.” It’s “I can sleep through a 40% equity market crash without touching this.”

Join The Global Frame

Money, work, and tech — one read every Saturday that actually changes how you think.

Short-term US Treasuries — T-bills in the one-to-three month range — are the core holding. Unlike corporate bonds, they carry no default risk in any meaningful sense. Unlike long-term Treasuries, they don’t get crushed by rising rates because they mature quickly and can be reinvested at current yields. At current rates, they’re generating returns that actually compete with inflation in a way they didn’t during the near-zero rate environment of the 2010s.

High-yield savings accounts and money market funds belong here too — not for return, but for liquidity. The investor with cash during a market crash isn’t just protecting themselves. They’re positioned to buy assets from people who need to sell. When HYSAs were paying 5%+, keeping a meaningful cash position wasn’t even a sacrifice. That window has narrowed as rates have come down, which is worth tracking actively, but the liquidity argument holds regardless of the yield.

Gold occupies a specific role on this side — not as an investment but as a hedge against the scenario where the currency itself is the problem. Central banks have been accumulating gold at record rates since 2022. That’s not a coincidence. It reflects institutional acknowledgment that fiat currency systems carry tail risks that most retail portfolios don’t account for. A 5-10% allocation to physical gold within the fortress acts as insurance against the specific scenario where everything else on this side also fails.

Paid-off real estate, if you’re there, functions as fortress capital too. Not as an investment vehicle — the rent-vs-buy math in 2026 is genuinely complicated and owning doesn’t automatically win — but as a reduction in monthly obligations that makes the rest of the fortress more resilient. A paid-off house in a stable market means your baseline survival cost drops significantly, which extends how long the fortress can sustain you without needing to touch anything else.

The Aggressive Side: Small Size, Genuine Asymmetry

The other 10% is where the strategy requires the most honesty with yourself, because the natural tendency is to fill this side with things that feel risky but are actually just volatile versions of the same middle-ground assets you’re trying to avoid.

Buying a tech sector ETF because it “feels aggressive” doesn’t belong here. Adding a few individual growth stocks to your portfolio isn’t this. What belongs in the aggressive 10% are positions where the realistic downside is losing the entire allocation and the realistic upside is a return large enough to matter to your overall net worth — not 20% or 30%, but multiples.

Angel investing has historically been the clearest example of genuine asymmetry. Nine out of ten early-stage companies fail completely. The tenth can return 100x. That distribution — most positions go to zero, one changes everything — is exactly what the aggressive side is designed to hold. Platforms like AngelList have made this accessible below the accredited investor threshold in ways that didn’t exist a decade ago.

Long-dated options — LEAPS — offer a different version of the same asymmetry for public markets. Rather than buying 100 shares of a company at full price, you buy the right to purchase those shares at a fixed price two years from now, for a fraction of the cost. If the stock doesn’t move, you lose the premium. If the stock moves significantly, the leverage in the option structure amplifies the return dramatically. The math only works if you’re sizing these correctly — treating each position as a defined, limited loss — which is why they belong in a capped 10% allocation rather than as a primary strategy.

The one asymmetric bet that often gets overlooked in this framing: yourself. A $5,000 investment in a skill, a course, a business experiment, or a professional relationship has theoretically infinite upside. The fractional executive market, the solopreneur infrastructure that AI agents are making viable, the side hustle income streams that compound into something larger — all of these are asymmetric bets on human capital where the downside is capped and the upside isn’t. These fit the barbell structure as naturally as any financial instrument.

What Gets Eliminated

The middle is where the strategy requires the most discipline, because the assets that belong there feel reasonable and familiar.

Corporate bonds are the clearest example. They offer capped upside — the yield — with meaningful downside — default risk or rate-driven price decline. You’re accepting the risk profile of an equity in exchange for the return profile of cash. That’s a bad trade in the barbell framework. If you want safety, short-term Treasuries do it better. If you want upside, equities or asymmetric positions do it better.

High-dividend yield traps are similar. A stock yielding 8-9% in a market where similar-quality companies yield 3% is usually pricing in the expectation that the dividend will be cut or the share price will fall. You’re collecting small, predictable income while absorbing large, unpredictable capital loss. That’s the middle ground in its worst form.

Actively managed mutual funds that closely track an index while charging 1%+ in fees are the most straightforward cut. If you want broad market exposure — and within the barbell framework, some exposure to equity growth on the safe side makes sense through low-cost index funds — the cheapest passive vehicle available does the job without the friction cost.

How to Actually Move Toward This

The transition doesn’t happen overnight, and trying to do it quickly creates tax problems that offset much of the benefit.

The more practical path is forward allocation — where you put new money — rather than wholesale liquidation of existing positions. If you’re contributing to a 401(k) or adding to taxable accounts, start directing those flows toward the structure you’re building. Existing positions can shift gradually, especially during rebalancing events or when you have losses to harvest for tax purposes.

The rebalancing rule on the aggressive side is the discipline that keeps the whole structure functional. When an asymmetric position wins — when that 10% allocation grows to 20% of your portfolio because something worked — you harvest the gains and move them to the fortress. You don’t let the risky side grow unchecked. The volatility on the aggressive side is supposed to feed the safety of the fortress, not gradually convert the whole portfolio into speculation.

This is also where the tax-advantaged account structure matters. Running barbell rebalancing inside a Roth IRA or HSA means the gains from asymmetric positions move to the fortress without a tax event. Outside of tax-advantaged accounts, frequent rebalancing has a cost. Building the aggressive side inside accounts where you can convert gains to safe holdings cleanly is worth planning deliberately.

The Honest Case for Doing Nothing Different

I want to acknowledge the legitimate counterargument before closing, because it exists and it’s not stupid.

The 60/40 portfolio failed in 2022. It had failed before in inflationary regimes. But across long holding periods — 20 years or more — broad equity exposure has compounded at rates that are genuinely difficult to beat on a risk-adjusted basis. The compound interest math for someone who stayed invested in a simple index strategy through every crisis from 2000 to 2025 is strong. The DCA evidence across market crashes supports staying in rather than trying to be clever about positioning.

The barbell isn’t a replacement for long-term equity exposure for every investor. It’s a framework for investors who are either closer to needing their money — where a 40% drawdown at the wrong time is catastrophic — or who have the financial stability to genuinely deploy aggressive capital knowing it might go to zero. For someone early in their career with stable income, decades of runway, and no dependents, a simple low-cost index strategy may well outperform a barbell over the full period.

The argument for the barbell gets stronger as your net worth grows, your time horizon shortens, and your interest in active participation in asymmetric opportunities increases. It also gets stronger in macroeconomic environments where the negative correlation between stocks and bonds can’t be assumed — which describes 2026 better than it described 2010.

The 60/40 had a good forty-year run. The conditions that made it work are gone. What you hold instead is your call — but “I haven’t decided yet” is still a decision. Just a passive one.