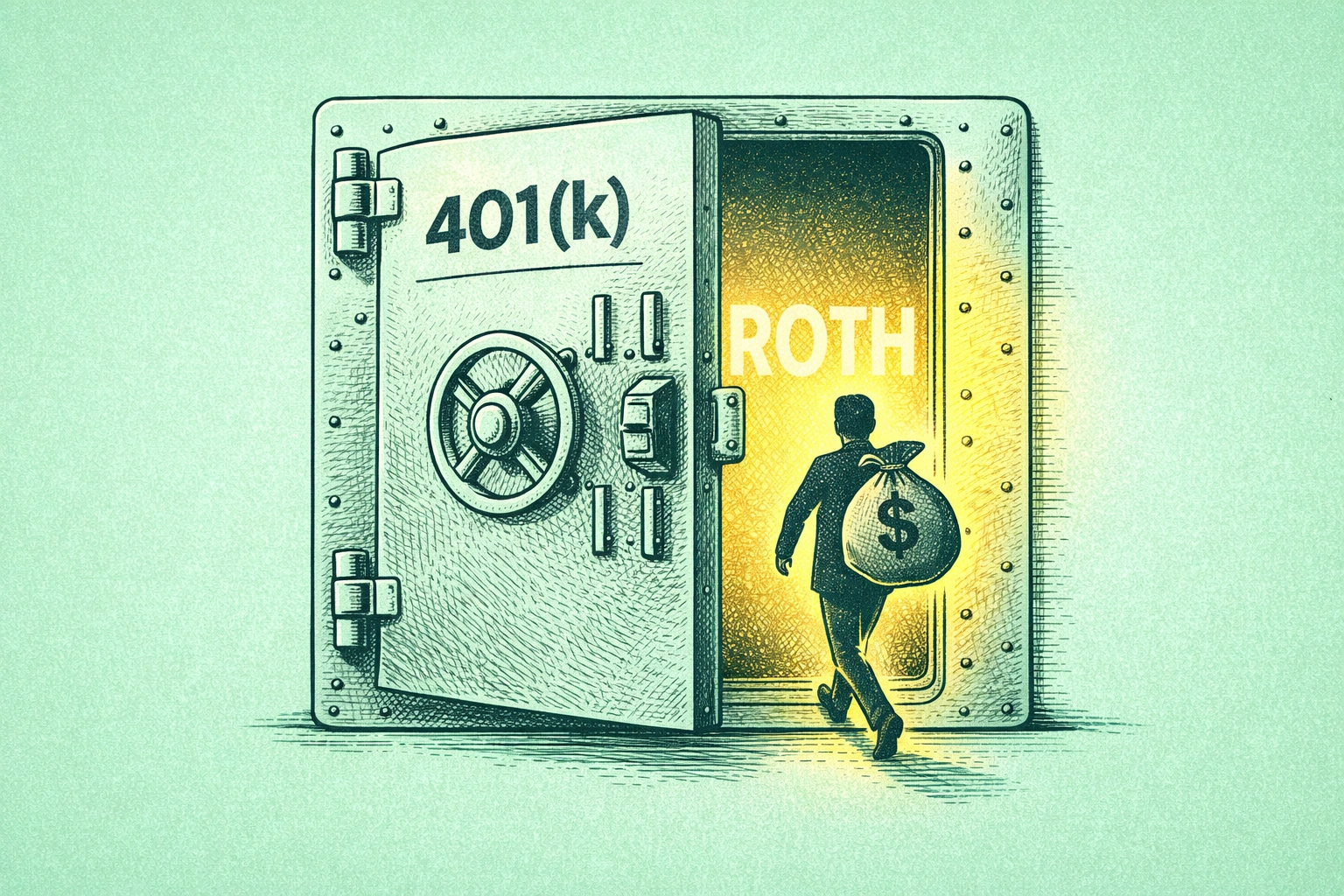

The mega backdoor Roth exists because the tax code has a gap in it, and the gap is large enough to drive a significant amount of money through. Most high earners hit the standard $24,500 401(k) contribution limit sometime in spring, assume they’re done for the year, and move on. They’re not done. They’re standing in front of a door they don’t know is open, one that leads to an additional $47,500 in Roth contributions — completely legal, available right now, and probably going away within a few budget cycles once Congress gets around to closing it.

The strategy works by exploiting the gap between what the IRS allows employees to contribute to a 401(k) ($24,500 in employee deferrals in 2026) and what it allows to enter the plan in total from all sources combined ($72,000). The space between those two numbers — minus your employer’s match — belongs to after-tax contributions that aren’t subject to income limits and, crucially, can be converted to Roth. The IRS confirms these limits annually in Notice 2025-67. The math for a typical tech employee: $72,000 total cap, minus $24,500 in deferrals, minus a $9,000 employer match on a $150,000 salary, leaves $38,500 in after-tax contribution space. Contribute that amount, convert it to Roth immediately, and you’ve added $38,500 to a tax-free account in a single year. Do it for five consecutive years and you’ve built a $192,500 Roth position — at 7% annual return over 30 years, that compounds to roughly $1.5 million you’ll never pay taxes on at withdrawal.

The Two Things Your Plan Must Allow

This is where most people’s eligibility ends before it begins. The mega backdoor Roth requires two specific features that the majority of 401(k) plans — particularly at smaller companies — simply don’t offer. Your plan must permit after-tax contributions beyond the standard employee deferral limit, and it must allow either in-plan Roth conversions or in-service withdrawals that let you roll those after-tax dollars to a Roth IRA while still employed. Without both, after-tax contributions just accumulate taxable earnings inside the plan with no clean path to Roth treatment.

Large employers — particularly in tech — are most likely to have both. Google, Microsoft, Apple, Amazon, Meta, Nvidia, and most Fortune 500 companies with competitive benefits packages tend to support the full mechanism. The reason smaller companies rarely offer it isn’t generosity — it’s IRS non-discrimination testing. The Actual Contribution Percentage test requires that highly compensated employees (anyone earning over $160,000 in 2026) don’t benefit disproportionately relative to everyone else in the plan. At a small company where most employees don’t max their basic contributions, the test frequently fails and the after-tax contributions get refunded. The strategy becomes unavailable not because of policy but because the math doesn’t clear compliance.

The fastest way to find out where you stand: call your HR department and ask specifically whether your plan allows after-tax contributions and in-service Roth conversions. Don’t use the phrase “mega backdoor Roth” — they may not recognize it. Get the answer in writing if you can, then verify by logging into your 401(k) provider’s portal and checking contribution election options. If “after-tax” appears as a contribution type alongside pre-tax and Roth, you’re likely eligible.

Executing It Without Triggering the Tax Landmines

The mechanics are straightforward once you confirm eligibility, but two technical details determine whether the conversion is genuinely tax-free or partially taxable. The first is timing. After-tax contributions accumulate earnings from the moment they land in the plan, and those earnings are taxable when converted to Roth — only the principal carries over tax-free. Converting within days of each contribution keeps the taxable portion negligible. Some plans offer automatic Roth conversion (sometimes called a “Roth sweep”), which handles this continuously. If yours does, turn it on. If not, log in and convert manually after each paycheck contribution rather than letting the balance build.

The second is the pro-rata rule, which applies specifically if you’re also running a regular backdoor Roth IRA alongside this strategy. If you hold pre-tax money in traditional IRAs — SEP-IRAs, SIMPLE IRAs, or rollover IRAs from old jobs — the IRS treats all your IRA money as a single pool when calculating the taxable portion of any conversion. A $100,000 traditional IRA balance alongside a $7,500 non-deductible contribution means roughly 93% of your backdoor Roth conversion is taxable, not zero. The fix: roll old traditional IRA balances into your current employer’s 401(k) before the conversion. Not all plans accept incoming rollovers, but many do, and it’s worth confirming before you’re surprised at tax time.

The step-by-step for 2026 runs in this order: max your standard deferrals first ($24,500, or $32,500 if you’re 50 or older, or $35,750 if you’re between 60 and 63 under SECURE 2.0), calculate your remaining after-tax space using the $72,000 minus deferrals minus employer match formula, elect after-tax payroll deductions across your remaining paychecks to spread the cash flow, then convert to Roth immediately after each contribution lands. For most people on a 26-paycheck biweekly schedule with $38,500 in available space, that’s approximately $1,480 per paycheck in after-tax contributions.

On the destination question: after-tax contributions can convert to either a Roth 401(k) inside your plan or roll out to a Roth IRA. The Roth IRA route is generally preferable. It removes the money from your employer’s plan entirely — giving you full investment flexibility beyond whatever options your plan offers — and Roth IRAs are not subject to required minimum distributions at 73 the way Roth 401(k)s are. You can also withdraw Roth IRA contributions (not earnings) at any time without penalty, which the 401(k) version doesn’t allow before 59½.

One structural consideration worth understanding: the mega backdoor Roth works best as part of a broader tax diversification approach. Concentrating all retirement savings in Roth accounts is as blunt as concentrating everything pre-tax. The barbell logic applied to retirement accounts — meaningful positions in both tax-free Roth and tax-deferred traditional space, with a clear plan for which bucket to draw from in which tax environment during retirement — produces more flexibility than optimizing for any single account type. And if you have access to a high-deductible health plan, maxing your HSA alongside this strategy adds a third tax treatment — the only account that’s deductible going in, tax-free growing, and tax-free coming out for medical expenses — that no combination of 401(k) and Roth IRA can replicate.

Join The Global Frame

Money, work, and tech — one read every Saturday that actually changes how you think.

Congress has tried to eliminate the mega backdoor Roth twice in recent memory. The Build Back Better Act in 2021 came close. Similar proposals appear in every budget negotiation where high-income retirement advantages become politically visible. The strategy is legal now, available in 2026, and almost certainly impermanent. The practical implication is to use it aggressively while eligibility exists — money already in a Roth account isn’t affected by future legislation that blocks new contributions. If your plan allows it and your cash flow supports it, this is not a strategy to research indefinitely. The window is open. The question is whether you walk through it this year or read about it after it closes.