Part 3 of the Rational Compounding Framework

There’s a specific type of broke that doesn’t look broke.

Last month I saw a thread on Blind where a $350K Meta engineer was asking if they should sell their car to cover rent. The comments were split between “how is this possible” and people sharing similar stories. Turns out it’s more common than anyone wants to admit.

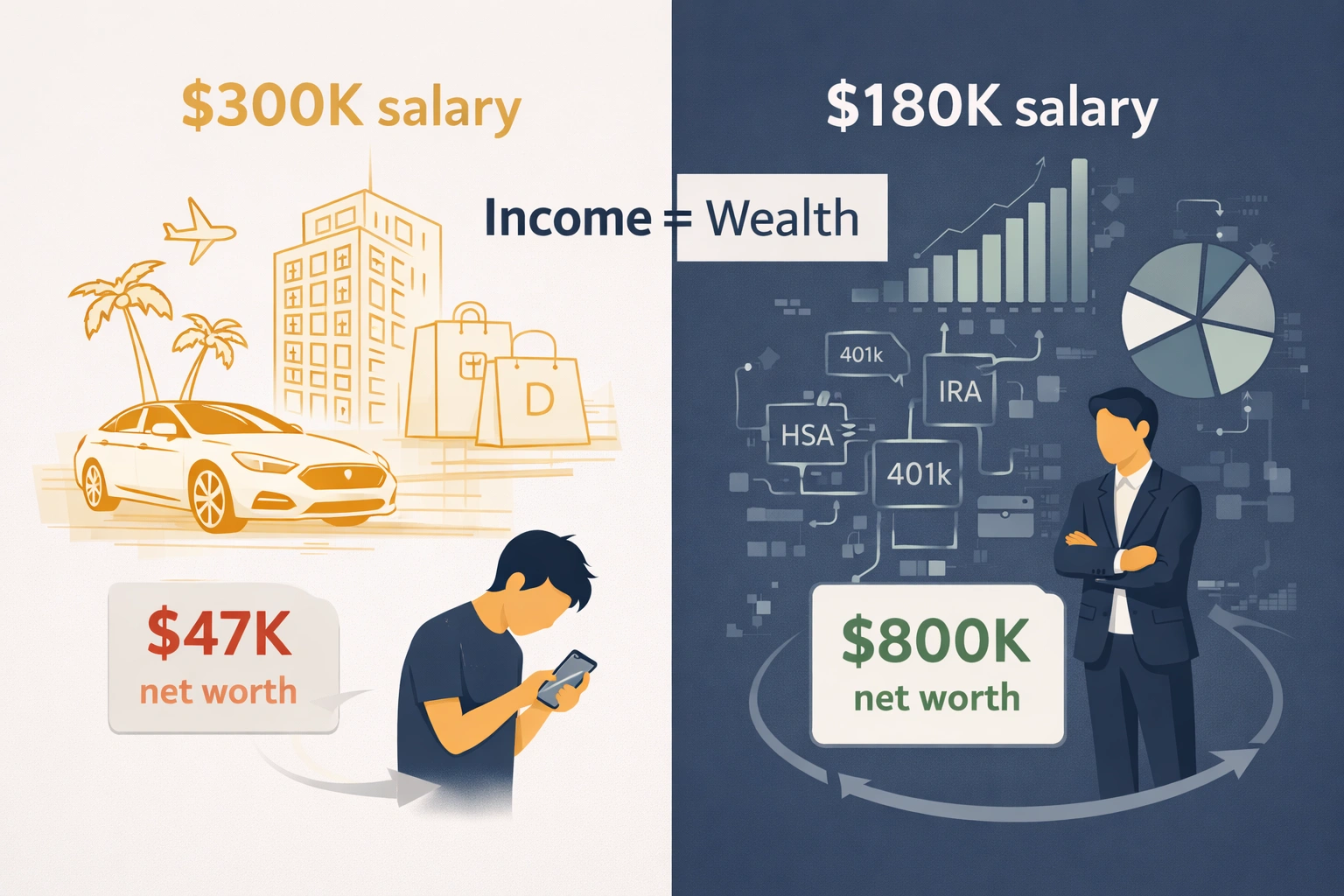

The $300K software engineer driving a leased Tesla, living in a $4,200/month apartment, taking two international vacations a year, ordering DoorDash four nights a week. Net worth at age 38: $47,000.

The $250K consultant with the designer wardrobe, the country club membership, the private school tuition sending their kids to. Net worth at 42: -$12,000. Student loans from Wharton, still paying them off.

These aren’t struggling people. They’re high earners with broken wealth engines.

They make more in a year than most households make in two or three. But ask them about their net worth and you’ll see confusion, then defensiveness, then deflection: “I’m investing in experiences.” “Life’s too short.” “I’ll catch up later.”

Later never comes. Because the problem isn’t income—it’s the four wealth killers that high earners either can’t see or refuse to acknowledge.

In Part 1, we covered the math of compounding. In Part 2, we broke down the three engines of wealth. Now let’s talk about why smart, high-earning people still end up with nothing.

This is the uncomfortable mirror.

The Four Wealth Killers

Wealth Killer #1: Lifestyle Inflation (The Silent Epidemic)

Here’s how it works:

You get promoted. Salary jumps from $120K to $150K. That’s $30K more per year—$19,500 after taxes.

What happens next is predictable:

The apartment search starts. “We can afford $800 more per month now.” The car lease feels justified—”I’m commuting to the office more, I need something reliable.” DoorDash stops feeling like a splurge when you’re working late. Vacations get booked to better destinations because “we earned this.” Subscriptions pile up—$150/month across fitness apps, streaming services, meal kits you barely use.

Add it up: $1,850/month in new expenses. $22,200/year.

Join The Global Frame

Money, AI, and career leverage. One email every Saturday to help you stay ahead of the curve.

Your after-tax raise was $19,500. Your new lifestyle costs $22,200.

You just got a raise and became poorer.

This is lifestyle inflation. And it’s not about being irresponsible. It’s about normalized spending creep that feels justified because “you can afford it now.”

The Real Numbers

Let’s compare two people over 20 years:

Person A: Lifestyle Scales with Income

- Age 30: Makes $120K, spends $90K, invests $30K (25%)

- Age 35: Makes $180K, spends $135K, invests $45K (25%)

- Age 40: Makes $250K, spends $200K, invests $50K (20%)

- Age 45: Makes $320K, spends $272K, invests $48K (15%)

- Age 50: Makes $380K, spends $342K, invests $38K (10%)

Average invested per year: $42,200

Total invested over 20 years: $844,000

Net worth at age 50 (at 8% returns): $2,051,489

Person B: Lifestyle Locks at Age 30 Level

- Age 30: Makes $120K, spends $90K, invests $30K (25%)

- Age 35: Makes $180K, spends $95K, invests $85K (47%)

- Age 40: Makes $250K, spends $100K, invests $150K (60%)

- Age 45: Makes $320K, spends $105K, invests $215K (67%)

- Age 50: Makes $380K, spends $110K, invests $270K (71%)

Average invested per year: $150,000

Total invested over 20 years: $3,000,000

Net worth at age 50 (at 8% returns): $7,309,573

Person B has $5.26 million MORE wealth.

Not because they earned more. Because they didn’t let lifestyle scale with income.

Why Smart People Fall for This

Lifestyle inflation feels rational in the moment:

- “I work hard, I deserve this.”

- “Everyone at my level has this.”

- “It’s only $200 more per month.”

And all of that is true. But wealth isn’t built on “deserving” things. It’s built on deploying capital systematically.

The $380K earner spending $342K has $38K deployable capital.

The $200K earner spending $110K has $90K deployable capital.

Lower income. Higher wealth. Every single time.

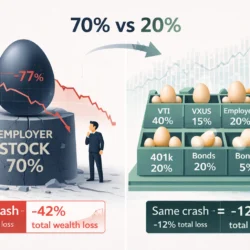

Wealth Killer #2: Concentration Risk (All Eggs in the Employer Basket)

Tech workers are especially vulnerable to this.

Your employer pays you in RSUs. Over 5 years, those vest and compound. The stock does well. You watch your “net worth” on Personal Capital climb. 60-80% of it is your employer’s stock, but that’s fine—everyone you know is in the same situation.

Then 2022 happens. Meta drops 70%. Your net worth drops $400K overnight. You can’t sell easily—there are tax implications, vesting schedules, psychological attachment (“it’ll come back”). So you ride it down, hoping for recovery.

One person I know went from a $950K net worth in October 2021 to $380K in October 2022. Same job. Same salary. Their wealth just… evaporated.

This isn’t wealth. This is concentrated risk masquerading as wealth.

The Brutal Math

Let’s say you have:

- $800K in employer stock

- $150K in diversified investments (401k, IRA)

- $50K emergency fund

Total net worth: $1 million

Employer stock drops 50% (not uncommon—see Meta 2022, Tesla 2022, Amazon 2022):

- Employer stock: Now $400K

- Diversified investments: Still $150K

- Emergency fund: Still $50K

New net worth: $600K

You just lost 40% of your wealth because of one company.

Now imagine you had:

- $200K in employer stock (20% of portfolio)

- $750K in diversified investments

- $50K emergency fund

Same 50% drop:

- Employer stock: Now $100K (-$100K)

- Diversified investments: Still $750K

- Emergency fund: Still $50K

New net worth: $900K

You lost 10% instead of 40%.

The 20% Rule

No single stock—especially your employer—should ever be more than 20% of your invested assets.

If it crosses 20%, you sell. Immediately. Tax hit be damned.

A 35% capital gains tax on $200K of gains is $70K.

Losing 50% of $800K is $400K.

Pay the $70K tax. It’s insurance against the $400K loss.

High earners resist this because they tell themselves stories:

“My company is different”—except it’s not. Every company looks unshakeable until it isn’t.

“I have insider knowledge”—which doesn’t protect you when the entire tech sector drops 40% or the Fed raises rates.

“I’ll sell when it hits $X”—but X never comes. Or when it does, you move the goalpost higher.

You’re either diversifying or you’re gambling. There’s no middle ground.

Wealth Killer #3: Tax Drag (Paying 10-15% More Than Necessary)

Most high earners pay a 32-37% effective tax rate.

Optimized high earners pay 22-28%.

That’s a 10-15 percentage point difference. On a $300K income, that’s $30K-45K per year.

Over 20 years? $600K to $900K in lost wealth.

Where the Leak Happens

Mistake 1: Not Maxing Tax-Advantaged Accounts

Available tax-advantaged space for a high earner in 2026:

- 401k: $23,500

- Backdoor Roth IRA: $7,000

- HSA: $4,300 (individual) or $8,550 (family)

- Mega Backdoor Roth: Up to $46,000 (if plan allows)

Total possible: $40,800 to $77,050 per year

Most high earners max the 401k ($23,500) and stop.

They’re leaving $17,300 to $53,550 in tax-advantaged space unused.

That money goes into taxable brokerage accounts where:

- Dividends are taxed annually

- Capital gains are taxed at 15-20%

- No Roth growth (tax-free forever)

Mistake 2: Ignoring State Tax Arbitrage

A $300K earner in California pays:

- Federal: ~$66,000

- State: ~$24,000

- Total: $90,000 (30% effective rate)

Same earner in Texas or Florida:

- Federal: ~$66,000

- State: $0

- Total: $66,000 (22% effective rate)

That’s $24,000/year saved. Over 20 years: $480,000.

Look, I’m not saying everyone should move to Austin or Miami. If you love where you live and you’re intentionally choosing to pay the premium, that’s fine. But if you’re remote anyway and you’re paying $24K/year in state taxes without even thinking about it? At least run the numbers with our relocation calculator.

Half a million dollars buys a lot of flights back to visit.

Mistake 3: Not Harvesting Losses

Tax-loss harvesting lets you offset gains with losses, reducing your tax bill.

Done systematically, this saves $2,000-5,000/year for a high earner with a $500K+ portfolio.

Over 20 years: $40,000-100,000 in tax savings.

Most people don’t do it because:

- They don’t know it exists

- They think it’s “advanced” (it’s not—robo-advisors do it automatically)

- They’re too lazy to set it up

Read our tax-loss harvesting guide if you’re leaving this money on the table.

The Tax Optimization Checklist

If you’re a high earner and you answer “no” to any of these, you’re overpaying:

- Maxing 401k ($23,500)

- Doing backdoor Roth IRA ($7,000)

- Maxing HSA and investing it ($4,300-8,550)

- Doing mega backdoor Roth if available (up to $46,000)

- Tax-loss harvesting in taxable accounts

- Considered state tax arbitrage for remote work

Every “no” is $3,000-10,000/year you’re giving to the IRS unnecessarily.

Wealth Killer #4: Ego Investing (Thinking You’re Smarter Than the Market)

Smart people are terrible investors.

Why? Because intelligence becomes a liability when it convinces you that you can beat the market.

You can’t. Neither can I. Neither can 95% of professional fund managers.

But high earners try anyway:

- Stock picking (“I work in tech, I know which companies will win”)

- Sector timing (“AI is the future, I’m going 100% tech”)

- Crypto gambling (“I got in early, I understand the space”)

- Individual real estate deals (“I found an undervalued property”)

Sometimes it works. Usually it doesn’t. And when it doesn’t, you lose years of compounding.

The Ego Tax

Let’s compare two investors over 10 years, both starting with $100K and adding $30K/year:

Investor A: Index Fund Boring

- Buys VTI (total stock market)

- Rebalances annually

- Ignores news

- 10-year return: 9.2% (historical average)

- Ending balance: $531,243

Investor B: Stock Picker Smart

- Picks 10-15 individual stocks

- Trades based on “research” and intuition

- Beats market some years, underperforms others

- 10-year return: 6.8% (average for active retail investors)

- Ending balance: $442,615

Investor A has $88,628 more.

Not because they were smarter. Because they were humble.

Why Smart People Fall for This

Ego investing feels like using your unfair advantage:

You work in the industry—you think you have insights others don’t. You’re analytical, you can spot patterns that retail investors miss. And hey, you’ve done pretty well so far betting on tech.

All of that might even be true. But here’s what’s also true:

Having insight doesn’t mean you can time the market. Being smart doesn’t automatically make you a good investor. And past success? The graveyard of failed investors is full of people who did well until they didn’t.

The market is efficient enough that your edge—assuming you even have one—is marginal. And those marginal gains get eaten alive by transaction costs, taxes on frequent trading, emotional decisions during 30% drawdowns, and the opportunity cost of time spent researching instead of earning more.

The smartest investors are boring. Deliberately.

The Income Illusion: Why $300K Doesn’t Mean You’re Rich

Here’s the lie high earners tell themselves:

“I make $300K. I’m doing fine.”

Maybe. Maybe not. You’re making $300K, sure. But whether you’re actually “doing fine” depends entirely on what you’re doing with it.

Let’s break down what $300K actually looks like after reality hits:

Gross income: $300,000

Federal taxes (~24% effective): -$72,000

State taxes (CA, ~8%): -$24,000

FICA (Social Security + Medicare, ~7%): -$21,000

After-tax income: $183,000

Now lifestyle:

- Rent/mortgage: $4,000/month = $48,000/year

- Car payment + insurance: $800/month = $9,600/year

- Food (groceries + dining): $1,500/month = $18,000/year

- Childcare (if applicable): $2,000/month = $24,000/year

- Health insurance premiums: $500/month = $6,000/year

- Utilities + subscriptions: $400/month = $4,800/year

- Travel + entertainment: $800/month = $9,600/year

- Misc/buffer: $1,000/month = $12,000/year

Total lifestyle: $132,000

Deployable capital: $51,000 (17% of gross)

That’s it. That’s what’s left to invest.

If you’re maxing your 401k ($23,500), backdoor Roth ($7,000), and HSA ($8,550), you’ve used $39,050 of that.

You have $11,950 left for taxable investing, emergency fund building, or opportunity capital.

And that assumes:

- No student loans

- No consumer debt

- No unexpected expenses

- No lifestyle inflation beyond this baseline

Making $300K doesn’t make you rich. It gives you the opportunity to become rich if you deploy capital systematically.

Most don’t. They let the $51K deployable capital get absorbed by:

- Slightly nicer apartment ($500/month more)

- Fancier car ($300/month more)

- Better vacations ($200/month more)

- “Life upgrades” ($500/month more)

And suddenly deployable capital is $33,000. Then $20,000. Then $8,000.

That’s why high earners stay broke.

How High Earners Should Actually Build Wealth

If you’re making $200K-500K and you’re not building wealth, here’s the system:

Step 1: Lock Your Lifestyle (The Non-Negotiable)

Pick a number. Say $120K/year all-in lifestyle.

Every raise, every bonus, every windfall—lifestyle stays at $120K.

Everything above that? Deployed capital.

This is hard because:

- Your peers are upgrading

- You feel like you’re “behind”

- Society tells you success = lifestyle

Ignore it. Wealth is invisible. Lifestyle is not.

The person driving the Tesla might have $30K net worth. The person driving the 10-year-old Honda might have $2 million invested.

Step 2: Max Every Tax-Advantaged Dollar

Before you invest a single dollar in taxable accounts:

- Max 401k: $23,500

- Max HSA: $4,300-8,550

- Do backdoor Roth: $7,000

- Do mega backdoor Roth if available: Up to $46,000

If your plan doesn’t offer mega backdoor Roth, switch jobs or negotiate for it. That’s $46K/year in Roth space—$920,000 over 20 years in tax-free growth.

Step 3: Diversify Immediately

If more than 20% of your net worth is in employer stock, sell.

Yes, you’ll pay capital gains tax. Pay it.

Tax cost: 15-20% of gains

Concentration risk cost: Potential 50-70% portfolio wipe-out

The math is clear.

Step 4: Automate Everything

Don’t rely on discipline. Rely on systems.

- Paycheck hits → Auto-max 401k

- Paycheck hits → Auto-transfer to brokerage

- Brokerage → Auto-invest in index funds

- Once/year → Rebalance if allocation drifts >5%

Remove yourself from the loop. Emotion kills wealth.

Step 5: Ignore Your Peers

This is the hardest part.

Your colleagues are leasing $90K cars and taking $15K vacations to Positano while you’re driving a paid-off Accord. They’re talking about the Michelin-star restaurant they hit last weekend while you meal-prepped on Sunday. They look successful. You look… cheap?

Wrong framing.

They’re sitting on $50K net worth at age 40. You’re building $200K/year in investments.

In 10 years, they’ll have $400K and be “stuck”—can’t retire, can’t take risks, handcuffed to the job because their lifestyle is too expensive to walk away from.

You’ll have $2.8 million and actual options.

Delayed gratification isn’t sacrifice. It’s trading short-term appearance for long-term freedom.

The Tesla looks good at the stoplight. The $2.8 million portfolio feels better everywhere else.

The Uncomfortable Truth

High earners don’t fail to build wealth because they don’t make enough.

They fail because:

- They let lifestyle scale with income

- They concentrate risk in employer stock

- They overpay taxes by 10-15%

- They ego-invest and underperform

Fix these four things and wealth becomes inevitable.

Ignore them and you’ll be 50 years old making $400K with $200K net worth, wondering where it all went.

The math doesn’t lie. Your lifestyle does.

Why High Earners Fail: Summary

High earners fail to build wealth when they optimize their Income Engine but destroy their Investment and Optionality Engines through lifestyle inflation, concentration risk, tax inefficiency, and ego investing.

Wealth is not income. Wealth is deployed capital compounding over decades.

Next in the series: Part 4: The RSU Trap—When Employer Stock Becomes a Hidden Liability

(Link will be live after Post #4 publishes)

Action Items

This week:

- Calculate your lifestyle lock number: What’s the minimum annual spend you need to be content? Lock it. Never let it grow faster than 3-5%/year.

- Check employer stock concentration: If it’s over 20% of net worth, sell enough to get back to 20%. Pay the tax. It’s insurance.

- Audit tax optimization: Are you maxing all available space? If not, you’re giving the IRS $10K-30K/year unnecessarily.

The difference between a high-earning broke person and a wealthy person isn’t income.

It’s what they do with it.

This is Part 3 of the Rational Compounding Framework. Read Part 1: The Math of Wealth for compounding mathematics, Part 2: The 3 Engines for the wealth system, or see the complete framework.