Part 4 of the Rational Compounding Framework

A friend at Google had this realization last year.

He’d been there seven years. Diligent. Saved aggressively. Maxed his 401k. Put money in index funds. Did everything “right.” His Personal Capital dashboard showed $1.2 million net worth. He felt wealthy.

Then he actually looked at the breakdown:

- $780K in Google stock (65% of net worth)

- $320K in diversified investments (401k, IRA, index funds)

- $100K emergency fund

One company. Two-thirds of his wealth.

“But Google’s stable,” he told me. “It’s not going anywhere.”

I asked him: “What was Meta’s stock price in September 2021?”

“Like $380?”

“And in November 2022?”

Long pause. “$88.”

That’s a 77% drop. If you had $780K in Meta, you’d wake up with $179K.

This is the RSU trap. And if you work in tech, you’re probably in it right now.

What Are RSUs and Why Are They Risky?

Quick Answer:

How much RSU concentration is safe?

No more than 20% of your total investment portfolio. Anything above that creates significant concentration risk that can destroy wealth in a single quarter.

Restricted Stock Units (RSUs) are employer stock grants that vest over time, typically four years. They’re taxed as ordinary income when they vest, not capital gains. Most FAANG employees in Seattle and the Bay Area cross 60% employer stock exposure without realizing it—turning compensation into a concentration time bomb.

Join The Global Frame

Money, AI, and career leverage. One email every Saturday to help you stay ahead of the curve.

What Makes RSUs Dangerous (The Single Point of Failure Problem)

Restricted Stock Units feel like free money. Your employer gives you $200K in stock as part of your compensation. It vests over four years. The stock goes up. Your net worth climbs. Life is good.

But RSUs aren’t free money. They’re concentrated risk masquerading as compensation.

Here’s why they’re uniquely dangerous:

Risk Layer 1: Your Income Depends on This Company

This is what I call the Single Point of Failure Wealth Model.

Single Point of Failure Wealth Model:

When your income and net worth depend on the same company, a single event can destroy both simultaneously. You’re not diversified—you’re exposed.

If the company struggles:

- Your salary stops

- Your unvested RSUs might get canceled

- Your vested RSUs drop in value

- You lose income AND wealth simultaneously

This is called double exposure. Your paycheck and your portfolio are tied to the same entity.

When diversified investors lose their job, their 401k stays intact. When RSU-heavy employees lose their job, their wealth evaporates with their income.

That’s not diversification. That’s dependence.

Risk Layer 2: Vesting Schedules Create Forced Hodling

You can’t sell unvested RSUs. You’re locked in.

Standard vesting schedule: 25% each year over four years.

If you join at a $200 stock price and it drops to $100 by year two, you’re still sitting on unvested shares worth 50% less than when you started. You can’t exit. You just watch.

Risk Layer 3: Tax Treatment Traps You Further

When RSUs vest, they’re taxed as ordinary income, not capital gains.

Example:

- $100K of RSUs vest

- You’re in the 35% tax bracket (federal + state)

- You owe $35K in taxes

Here’s what actually happens:

Your brokerage (Fidelity, E*Trade, Morgan Stanley) automatically sells to cover the taxes. They withhold shares worth ~22% for federal taxes plus your state rate (often 25-28% total). The remaining shares land in your account.

But here’s the trap within the trap:

If you’re a high earner in the 32-37% federal bracket, the 22% withholding isn’t enough.

You vest $150K. The brokerage withholds $33K (22%). You think you’re done.

Come April, you owe another $19,500 in taxes because you were actually in the 35% bracket.

This surprise tax bill is why high earners often feel like they “can’t afford” to sell more shares—they’re already cash-strapped from the under-withholding.

The fix: Adjust your W-4 to increase withholding, or set aside cash from each vesting event for the April surprise.

The real trap: Because the brokerage handled everything automatically, you didn’t have to do anything. The shares just appeared. So you do… nothing.

You don’t sell. You don’t rebalance. You let them sit.

Batch after batch, quarter after quarter, the shares accumulate. Your concentration grows. You tell yourself “I’ll deal with it later.”

The IRS forces you to pay taxes on vesting. Your inertia forces you to become a gambler.

Risk Layer 4: Psychological Attachment

I’ve seen this play out dozens of times.

Someone joins a company at $100/share. It climbs to $300. Their RSUs are now worth 3x what they were granted. They feel smart. They feel like they “earned” those gains through loyalty and hard work.

When the stock drops to $200, they don’t sell. “It’s still up from my strike price.” When it drops to $150, they don’t sell. “It’ll come back.” When it drops to $80, they’re underwater and psychologically paralyzed.

You don’t divorce your employer’s stock. You’re emotionally married to it.

The Math That Tech Workers Refuse to Face

Let’s run the numbers on concentration risk.

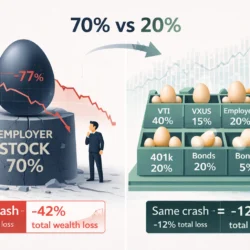

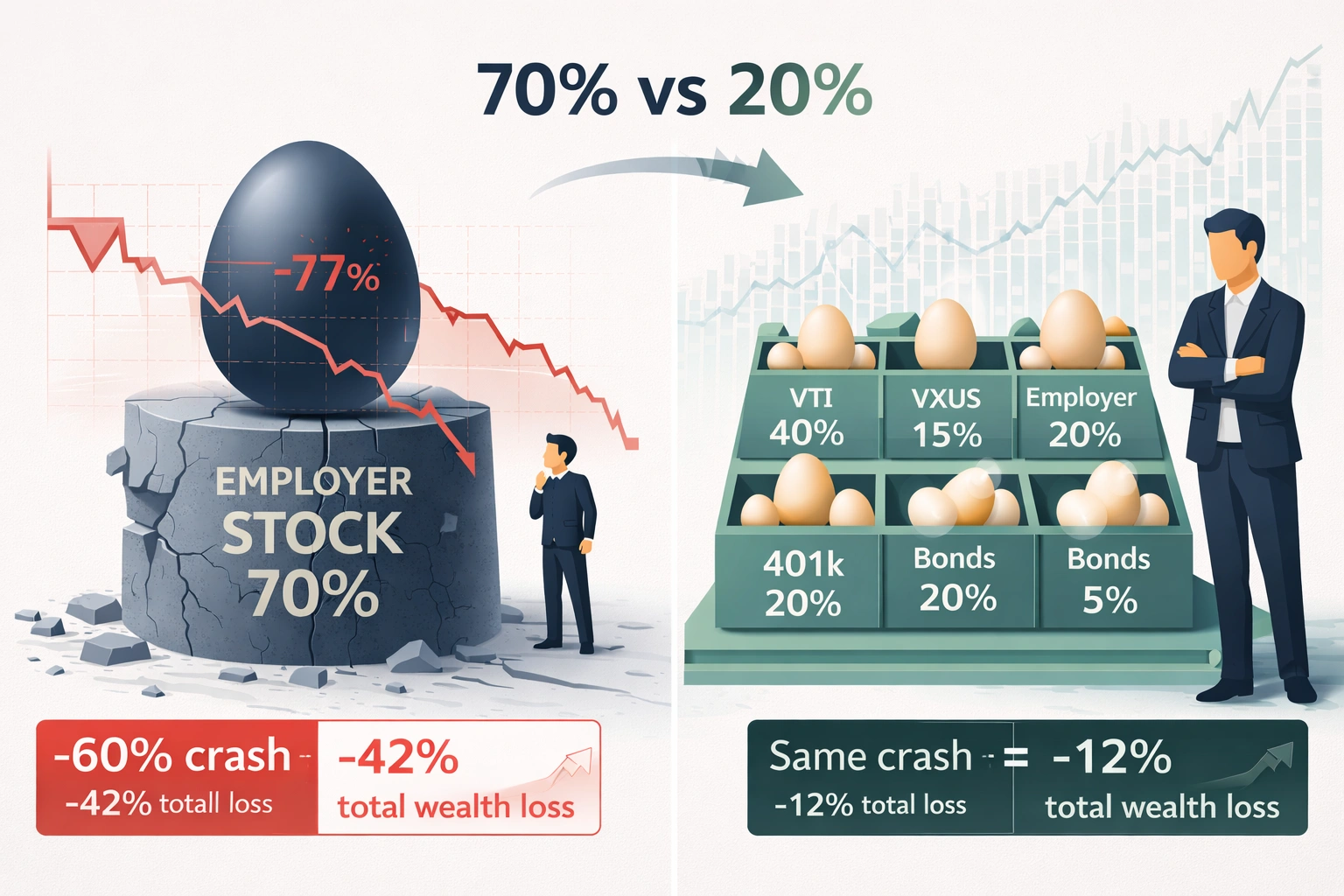

Scenario A: 70% Employer Stock (Typical Tech Worker)

Starting portfolio: $1 million

- $700K in employer stock

- $250K in diversified investments (401k, IRA)

- $50K cash

Employer stock drops 60% (not uncommon—see Meta 2022, PayPal 2022, Shopify 2022, Netflix 2022):

- Employer stock: $280K (-$420K)

- Diversified investments: $250K (unchanged)

- Cash: $50K (unchanged)

New net worth: $580K

You lost 42% of your wealth in one move you couldn’t control.

Scenario B: 20% Employer Stock (Diversified)

Starting portfolio: $1 million

- $200K in employer stock

- $750K in diversified investments

- $50K cash

Same 60% employer stock drop:

- Employer stock: $80K (-$120K)

- Diversified investments: $750K (unchanged)

- Cash: $50K (unchanged)

New net worth: $880K

You lost 12% instead of 42%.

The difference between Scenario A and Scenario B is $300,000 in wealth preservation.

And this isn’t hypothetical. This exact scenario played out in 2022 for thousands of tech workers at Meta, Netflix, Shopify, PayPal, Coinbase, Robinhood, and others.

What Actually Happened in 2022 (Tech Stock Drawdowns)

Here’s the data that tech workers don’t want to face:

| Company | Peak → Bottom | % Drop | Timeframe |

|---|---|---|---|

| Meta | $384 → $88 | -77% | Sep 2021 – Nov 2022 |

| Netflix | $700 → $175 | -75% | Nov 2021 – May 2022 |

| Shopify | $176 → $26 | -85% | Nov 2021 – Oct 2022 |

| PayPal | $310 → $67 | -78% | Jul 2021 – May 2022 |

| Amazon | $188 → $81 | -57% | Jul 2021 – Dec 2022 |

| $152 → $83 | -45% | Feb 2022 – Dec 2022 |

If you were 70% concentrated in any of these, you lost 50-60% of your total wealth in 12-18 months.

Not because you were bad at your job. Not because you spent recklessly. Because you violated The 20% Concentration Rule.

Real Examples: When the Single Point of Failure Model Collapses

Meta: The $950K to $380K Story

I mentioned this person in Part 3. Let me give you the full picture.

October 2021:

- Meta stock: $338

- This person’s portfolio: $950K (75% Meta stock, 25% other)

- Net worth: Top 5% for their age

October 2022:

- Meta stock: $97 (-71%)

- Same person’s portfolio: $380K

- Net worth: Cut in half, plus change

They lost $570,000 in twelve months.

Not because they were bad at their job. Not because they spent recklessly. Because they had all their eggs in one basket and Mark Zuckerberg decided to spend $10 billion on the metaverse while Apple kneecapped their ad business.

This is the Single Point of Failure Wealth Model in action. Your wealth shouldn’t depend on decisions you don’t control.

In the Bay Area, a $1M net worth isn’t financial freedom when 70% of it can vanish in one quarter.

Tesla: The Volatility Roller Coaster

Tesla is a cult stock, which makes it extra dangerous for employees.

November 2021: $414/share

December 2022: $123/share (-70%)

July 2023: $293/share (+138% from bottom)

April 2024: $175/share (-40% from peak)

If you’re a Tesla employee trying to build wealth, this volatility is a nightmare.

You vest shares at $400. They drop to $120. You can’t sell (psychological attachment + “it’ll come back”). They recover to $290. You still don’t sell (“maybe it’ll hit $400 again”). They drop to $175.

You rode a roller coaster for three years and ended up 57% below where you started.

Meanwhile, someone in index funds was up 25% over the same period.

You’re not investing. You’re exposed.

The Tax Trap: Why “Just Sell” Isn’t Simple

The most common pushback I hear: “If you don’t want concentration risk, just sell when RSUs vest.”

Sounds simple. It’s not.

The Vesting Tax Hit

When RSUs vest, they’re taxed as ordinary income at your marginal rate.

Example:

- Salary: $200K

- RSUs vesting this year: $150K

- Total income: $350K

- Tax bracket: 35% federal + 10% state = 45% effective

- Tax bill on RSUs: $67,500

Your employer typically withholds some shares to cover this (usually 22-25% federal). But that’s often not enough if you’re in a high tax state.

You vest $150K in stock. You get $112K worth of shares after withholding. You still owe an additional $22K at tax time.

The Double-Tax Problem

Now let’s say you hold those shares and they appreciate.

You received $150K worth of stock at vesting. It grows to $200K. You sell a year later.

Taxes owed:

- Already paid at vesting: $67,500 (ordinary income tax – 45% of $150K)

- Capital gains on $50K appreciation: $10K (20% long-term rate)

Total tax: $77,500 on $200K = 38.75% effective rate

Compare this to selling immediately on vest day:

- Tax owed: $67,500 (ordinary income on $150K)

- Capital gains tax: $0 (sold at cost basis)

- Total tax: $67,500 on $150K = 45% effective rate

You “saved” $10K by holding for a year and hoping for gains.

But you also:

- Took on 12 months of concentration risk

- Exposed yourself to potential 40-60% crashes

- Risked your principal to save 7.5% in taxes

Is that trade worth it?

Should You Sell RSUs Immediately?

Not necessarily 100%—but you should sell enough to stay under The 20% Concentration Rule.

Here’s the tax reality that destroys the most common objection:

If you sell RSUs on the day they vest, you pay ZERO capital gains tax.

Let me repeat that because most tech workers don’t understand this:

When RSUs vest at $100/share, you immediately owe income tax on $100/share. That’s done. Paid. The brokerage withheld it via sell-to-cover.

The $100 becomes your cost basis.

If you sell at $100 the same day, there’s no gain. No capital gains tax. You already paid the only tax you owe (income tax at vesting).

If you hold the stock and it goes to $120, then you sell, you pay:

- Income tax on $100 (already paid at vesting)

- Capital gains tax on the $20 gain

Holding the stock doesn’t save you from taxes. It just forces you to risk your principal for the chance to pay capital gains taxes later.

The “I don’t want to pay taxes” objection is based on a fundamental misunderstanding of how RSU taxation works.

Here’s why this matters more than the tax savings:

Is saving 7.5% in taxes worth risking a 60% drawdown?

For most people, no. But the tax pain of selling makes them hold. And holding concentrates risk.

The 20% Concentration Rule: Your Line in the Sand

Here’s the rule that will save you from this trap:

The 20% Concentration Rule:

No single stock—especially your employer’s—should ever exceed 20% of your invested assets.

Not 25%. Not 30%. Not “it depends.” Twenty percent. Hard stop.

How Much Employer Stock Is Too Much?

The math is brutal but simple:

Why 20%?

Because at 20%, a catastrophic 70% drop in that stock only costs you 14% of your total portfolio. That’s survivable.

At 50% concentration, a 70% drop costs you 35% of your total portfolio. That’s life-altering.

At 70% concentration (common for tech workers), a 70% drop costs you 49% of your wealth. That’s devastating.

How to Apply the 20% Rule

Before we get tactical, do a quick self-check right now:

RSU Concentration Self-Check:

- What % of your net worth is employer stock? (Calculate it now)

- When was the last time you sold RSUs? (Ever?)

- Do you have a systematic sell rule? (Or just vibes?)

If you answered “I don’t know,” “Never,” or “No,” keep reading.

Step 1: Calculate Current Concentration

Formula: (Employer Stock Value / Total Invested Assets) × 100

Example:

- Employer stock: $500K

- 401k: $200K

- IRA: $50K

- Taxable brokerage: $150K

- Total invested: $900K

Concentration: $500K / $900K = 55.5%

You’re at nearly 3x the safe limit.

Step 2: Set Your Target

Target employer stock value: $900K × 20% = $180K

Amount to sell: $500K – $180K = $320K

Step 3: Execute the Sale

Sell $320K worth of employer stock. Now.

Yes, you’ll pay capital gains tax (15-20% federal + state).

On $320K sale with $100K in gains: ~$30K tax bill.

You just paid $30K for diversification insurance that protects $400K+ in downside risk.

That’s the trade. Take it.

Step 4: Rebalance Quarterly

As new RSUs vest, sell enough to maintain 20% concentration.

Every quarter:

- Calculate current concentration

- If >25%, sell down to 20%

- Reinvest proceeds in diversified index funds

This becomes automatic. Emotion-free. Systematic.

What to Do With the Proceeds

After you sell employer stock, you need a plan for the cash.

Bad move: Leave it in cash earning 4%

Good move: Immediately redeploy into diversified investments

Here’s the priority:

Priority 1: Max Tax-Advantaged Space

Before you invest in taxable accounts:

- Max 401k: $23,500

- Max backdoor Roth: $7,000

- Max HSA: $4,300-$8,550

- Max mega backdoor Roth if available: Up to $46,000

Read our guides on backdoor Roth, mega backdoor Roth, and HSA strategies if you’re not maxing these.

Priority 2: Taxable Brokerage in Index Funds

After maxing tax-advantaged space, use taxable brokerage accounts:

- 70% total US stock market (VTI, VTSAX)

- 20% international (VXUS, VTIAX)

- 10% bonds if over 40 years old (BND, VBTLX)

Keep expense ratios under 0.1%. Rebalance annually.

Priority 3: Tax-Loss Harvesting (With a Critical Warning)

If you’re selling employer stock at a gain, pair it with tax-loss harvesting in your taxable accounts to offset gains and reduce your tax bill.

BUT: Critical warning for RSU holders.

If you’re trying to tax-loss harvest by selling older employer stock at a loss, you must check your RSU vesting schedule first.

The Wash Sale Rule: If you have new RSUs vesting within 30 days (before or after) of selling old shares at a loss, the IRS disallows the loss deduction. It gets rolled into the cost basis of the new shares instead.

Since most tech workers vest monthly or quarterly, you’re constantly in a 30-day window.

Translation: Tax-loss harvesting employer stock is extremely difficult if you have ongoing RSU vesting.

If you want to harvest losses, you need to either:

- Sell positions in other stocks (not your employer)

- Stop your RSU vesting schedule (not realistic)

- Accept that you can’t harvest employer stock losses

This is another reason to diversify out of employer stock immediately when it vests—it keeps your tax situation clean.

The Systematic RSU Sale Strategy

Here’s the system that removes emotion from the equation:

On Vesting Day (Automatic)

Sell 50-70% immediately.

Why not 100%? Because of taxes and psychology.

Selling 50-70% gives you:

- Immediate diversification

- Tax payment covered

- Some upside exposure if the stock runs

If you vest $100K:

- Sell $60K immediately → diversify

- Keep $40K in employer stock

- Monitor quarterly for rebalancing

Quarterly Review (Scheduled)

Set a calendar reminder: First Monday of each quarter.

Check concentration:

- If employer stock >25% of portfolio → Sell down to 20%

- If employer stock <15% of portfolio → You can let it ride

- If employer stock 15-25% → No action needed

This takes 15 minutes every 90 days.

Annual Tax-Optimization Review

Once per year (January):

- Review total tax bill from RSU vesting

- Adjust withholding if needed for next year

- Confirm you’re maximizing all tax-advantaged accounts

- Consider tax-loss harvesting opportunities

Common Objections (And Why They’re Wrong)

“But My Company is Different”

No, it’s not.

Most tech employees aren’t investors. They’re concentrated shareholders who got lucky—until they didn’t.

Google employees said this. Amazon employees said this. Meta employees said this. Netflix employees said this.

Then:

- Google dropped 45% in 2022

- Amazon dropped 55% in 2022

- Meta dropped 77% in 2022

- Netflix dropped 75% in 2022

High earners in Seattle and SF crossed 60% employer exposure without noticing. Then 2022 hit.

Every company is one bad quarter, one CEO decision, one regulatory change, or one macro shift away from a 50%+ drawdown.

“I Have Insider Knowledge”

Insider knowledge helps you understand your company’s business. It doesn’t protect you from:

- Macro crashes (2022)

- Sector rotation (tech to energy in 2022)

- Multiple compression (valuations collapsing)

- Fed policy (rate hikes crushing growth stocks)

You can have perfect insight into your company and still lose 60% of your wealth when the entire tech sector crashes.

“I’ll Sell When It Hits $X”

This is the most dangerous lie tech workers tell themselves.

The stock is at $200. You’ll sell at $250.

It hits $250. You don’t sell. “Maybe it’ll hit $300.”

It hits $300. You don’t sell. “Maybe it’ll hit $400.”

It drops to $200. You don’t sell. “I’ll wait for it to get back to $300.”

It drops to $100. You’re paralyzed.

Moving goalposts is how you ride stocks down to zero.

The only rule that works: Follow The 20% Concentration Rule. No exceptions.

This is how people lose years of progress in one quarter.

“The Tax Hit is Too Big”

This objection is based on a misunderstanding.

Let’s be crystal clear:

Selling on vest day = $0 capital gains tax.

You already paid income tax when the RSUs vested. That’s done. The only “new” tax you’d pay is capital gains on any appreciation after vesting.

So let’s do the math on the actual scenario:

You have $500K in employer stock with $200K in gains (meaning you received $300K at vesting, it grew to $500K).

Tax bill if you sell now:

- Income tax: Already paid when it vested ($135K at 45% on $300K)

- Capital gains on $200K gain: ~$40K (20% federal + state)

Total new tax owed: $40K

You keep: $460K to diversify

Alternative: Hold and risk a 60% crash

Loss from 60% crash: $500K × 60% = $300K

You’d rather risk losing $300K than pay $40K in taxes?

The tax objection is emotional, not rational.

And if you’re worried about taxes eating into gains, remember: You only pay capital gains if the stock went up. If it crashes, you paid zero capital gains and you lost your principal.

Pay the tax. Protect the wealth.

What Concentration Risk Actually Costs You

Let’s look at the long-term impact of staying concentrated.

Person A: Stays 70% Concentrated in Employer Stock

Starting at age 30 with $200K:

- Adds $50K/year

- Stays 70% employer stock, 30% diversified

- Employer stock returns: 12% some years, -40% other years (volatile)

- Average return over 20 years: 8%

Age 50 net worth: $2.1 million

But the journey included:

- Three separate 50%+ crashes

- Sleepless nights during volatility

- Nearly getting wiped out in 2022

Person B: Maintains 20% Concentration, Rebalances Quarterly

Starting at age 30 with $200K:

- Adds $50K/year

- Maintains 20% employer stock, 80% diversified

- Diversified returns: 9% consistently (index funds)

Age 50 net worth: $2.5 million

Person B has $400K more wealth AND slept better for 20 years.

The concentrated position doesn’t even win. It just adds risk.

What I’ve Seen From the Hiring Side

I’ve interviewed and hired hundreds of tech workers over the years. Here’s the pattern I see repeatedly:

The overconfident high earner:

- Makes $300K-500K

- Feels wealthy because of high income

- Has 60-80% net worth in employer stock

- Thinks “my company is different”

- Ignores concentration risk entirely

The wake-up call:

- Stock drops 40-60% in a correction

- Net worth cut in half

- Suddenly realizes wealth was an illusion

- But still doesn’t sell (waiting for recovery)

Most high earners don’t treat RSUs as risk. They treat them as proof of success. That’s the trap.

Your wealth shouldn’t be tied to one company’s stock performance. Especially not the company that also pays your salary.

How to Fix This Starting Tomorrow

If you’re sitting on concentrated employer stock right now, here’s your action plan:

Tomorrow Morning:

- Calculate your concentration percentage

- Open Personal Capital, Mint, or wherever you track net worth

- Divide employer stock by total invested assets

- If it’s >20%, you need to sell

- Open your brokerage account

- Find your employer stock holdings

- Calculate how much to sell to get to 20%

- Place the sell order

- Don’t overthink the timing

- You’re not selling because the stock is overvalued

- You’re selling because you’re over-concentrated

- Today is as good as any day

This Week:

- Reinvest the proceeds immediately

- Transfer to your 401k (if you can increase contributions)

- Fund your backdoor Roth ($7,000)

- Fund your HSA ($4,300-8,550)

- Put the rest in VTI or VTSAX in taxable brokerage

- Set a quarterly calendar reminder

- “Check RSU concentration”

- First Monday of Jan/Apr/Jul/Oct

- Review and rebalance if needed

This Month:

- Adjust your RSU vesting strategy

- Set automatic sells for 60% of vested RSUs going forward

- Keep 40% if you want some exposure

- Never let concentration creep above 25%

The Brutal Truth

RSUs are compensation, not investment strategy.

When your employer gives you $200K in stock, they’re not saying “we think you should have 70% of your wealth in our stock.”

They’re saying “here’s $200K worth of compensation, paid in stock for tax and retention reasons.”

Your job is to treat it like cash and diversify immediately.

Rich people don’t stay rich by being loyal to employer stock. They stay rich by protecting wealth through diversification.

The trap is thinking RSUs are special because you “earned” them. They’re not special. They’re just stock. And concentrated stock positions destroy wealth.

Follow The 20% Concentration Rule. Sell when you exceed it. Rebalance quarterly.

RSUs don’t make you wealthy. Managing them correctly does.

The RSU Trap: Summary

RSUs create a Single Point of Failure Wealth Model where your income and net worth depend on the same company. When concentrated above 20%, they create catastrophic downside exposure that no amount of upside can justify.

The solution is mechanical: Follow The 20% Concentration Rule—sell when concentration exceeds 20%, reinvest in diversified holdings, and rebalance quarterly. This is how you build wealth instead of gambling with it.

Next in the series: Part 5: Buy the Dip—But Only If You Have a Deployment System

(Link will be live after Post #5 publishes)

Action Items

This week:

- Calculate RSU concentration: Employer Stock / Total Invested Assets. If >20%, sell enough to get to 20%.

- Set automatic sells: Configure your brokerage to automatically sell 60% of vested RSUs going forward.

- Create quarterly calendar reminder: First Monday of every quarter, check concentration and rebalance if needed.

You didn’t build wealth to lose it on one stock. Diversify.

This is Part 4 of the Rational Compounding Framework. Read Part 1: The Math of Wealth, Part 2: The 3 Engines, Part 3: Why High Earners Fail, or see the complete framework.