Part 1 of the Rational Compounding Framework

There’s a scene that plays out every December in finance.

Someone at a holiday party mentions their portfolio is up 47% for the year. They bought NVIDIA at the right time, or rode some crypto wave, or nailed a tech stock before it doubled. The room goes quiet. Everyone feels a little behind.

Here’s what that conversation doesn’t include: what happened the other nine years. The positions that went to zero. The “sure things” that evaporated. The fact that their actual annualized return over a decade is 6%, not 47%.

Luck makes for good stories. Discipline makes for actual wealth.

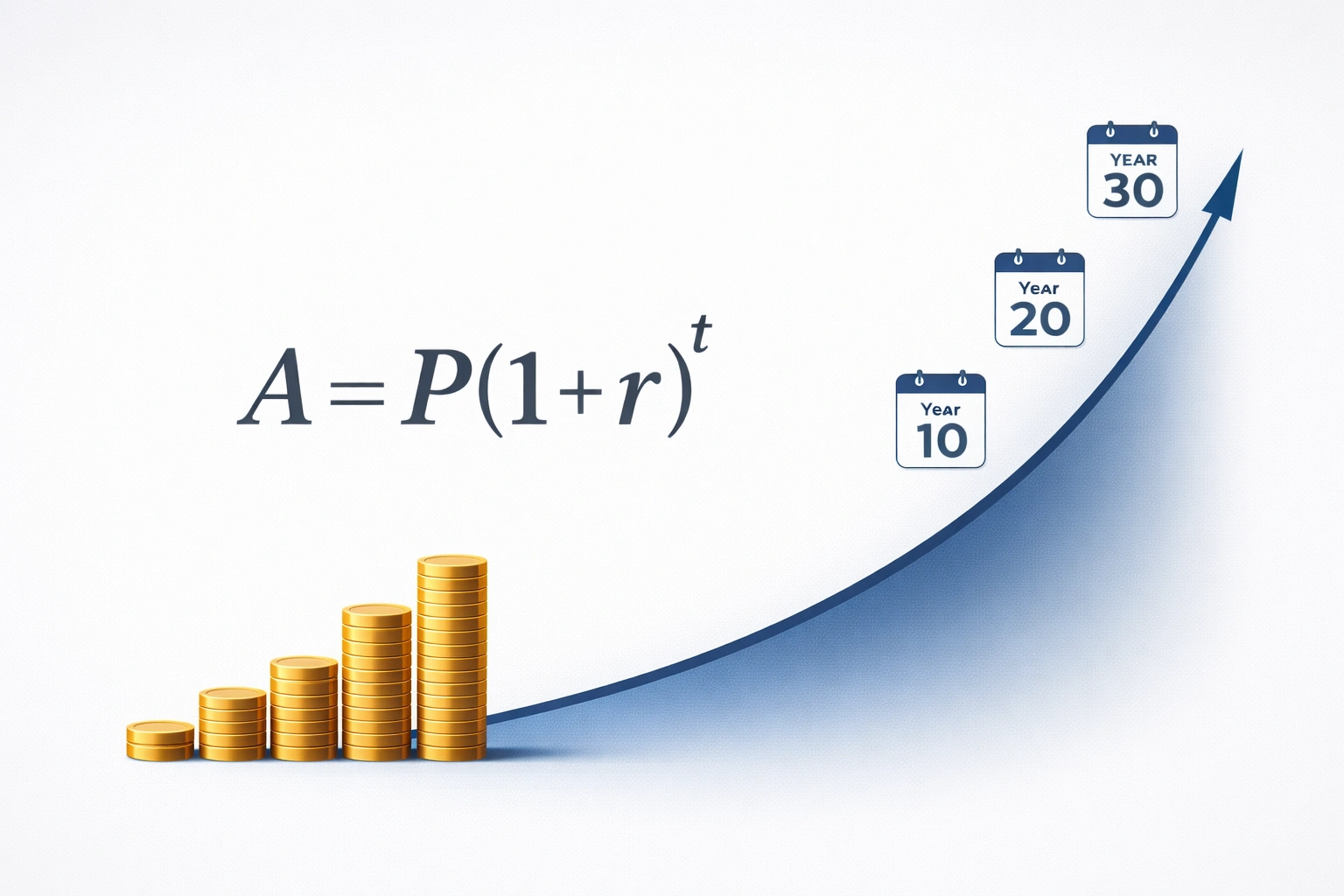

This is the foundational truth of wealth building, and it’s rooted in math that’s been known for 400 years but that most people still don’t internalize: A = P(1 + r)^t

Every dollar you invest grows as compound interest. Wealth isn’t about finding the magic 47% year. It’s about maximizing P (how much you deploy), protecting r (your returns), and extending t (time in the market).

Let me show you why the disciplined beat the lucky. Every single time.

The Difference Between Arithmetic and Geometric Returns

Most people think returns are additive. They’re not.

If you earn 50% one year and lose 50% the next, you’re not back to even. You’re down 25%.

Here’s the math:

- Start with $100,000

- Year 1: +50% = $150,000

- Year 2: -50% = $75,000

You lost $25,000.

This is why volatile returns destroy wealth even when they average out to something respectable.

The Volatility Tax

Let’s compare two investors over 10 years:

Investor A (The Lucky Gambler):

Join The Global Frame

Money, AI, and career leverage. One email every Saturday to help you stay ahead of the curve.

- Returns: +40%, -20%, +60%, -30%, +50%, -10%, +35%, -25%, +45%, -15%

- Arithmetic average: 13% per year

- Actual ending balance on $100K: $186,434

- Geometric average: 6.4% per year

Investor B (The Disciplined Indexer):

- Returns: +9%, +8%, +11%, +7%, +10%, +9%, +8%, +10%, +9%, +8%

- Arithmetic average: 8.9% per year

- Actual ending balance on $100K: $232,496

- Geometric average: 8.8% per year

Investor B made $46,062 more with lower average returns.

Why? Because consistency compounds. Volatility doesn’t.

The math is simple but brutal: sequence matters more than average.

Why 8% for 30 Years Beats 12% for 20 Years

This is the part that makes people’s eyes glaze over in finance 101. But understanding it changes everything.

Let’s say you have two scenarios:

Scenario 1: Start Early, Lower Returns

- Invest $10,000/year for 30 years

- Earn 8% annually

- Total contributions: $300,000

- Ending balance: $1,223,459

Scenario 2: Start Late, Higher Returns

- Invest $10,000/year for 20 years

- Earn 12% annually

- Total contributions: $200,000

- Ending balance: $806,987

Starting 10 years earlier with LOWER returns nets you an extra $416,472.

That’s the power of time. Not luck. Not superior stock picking. Time.

And here’s the kicker: the 8% scenario is more realistic. Consistent index fund returns over three decades tend to hover around 8-10%. The 12% scenario requires either exceptional market timing or concentrated bets that introduce massive risk.

The disciplined investor who starts at 25 beats the “smart” investor who starts at 35. Every time.

The Real Compounding Formula (And What It Actually Means)

Let’s break down A = P(1 + r)^t with real numbers.

Say you’re 30 years old. You have $50,000 saved. You can invest $2,000/month ($24,000/year). You plan to retire at 60.

Here’s what changes your outcome:

Variable 1: P (Principal + Contributions)

If you invest $24,000/year for 30 years at 8%:

- Total contributions: $720,000

- Ending balance: $2,977,075

If you invest $30,000/year (just $500 more per month):

- Total contributions: $900,000

- Ending balance: $3,721,344

$500/month more = $744,269 more wealth.

This is why increasing your savings rate by even 5-10% matters more than chasing an extra 1% in returns.

Variable 2: r (Returns)

Starting with $50,000, investing $24,000/year for 30 years:

At 6% returns: $2,124,860

At 8% returns: $2,977,075 (+$852,215)

At 10% returns: $4,129,920 (+$1,152,845)

Each 2% in returns is worth over $1 million.

But here’s the reality check: getting from 6% to 8% is achievable through basic tax optimization strategies and low-cost index funds. Getting from 8% to 10% requires either taking more risk or getting lucky with timing.

The disciplined move: Protect the 8% you can reliably achieve. Don’t chase the 10% that requires luck.

Variable 3: t (Time)

This is the most powerful variable, and the one you have the least control over once you start.

Starting with $50,000, investing $24,000/year at 8%:

After 20 years: $1,295,283

After 30 years: $2,977,075 (+$1,681,792)

After 40 years: $6,617,527 (+$3,640,452)

Every additional decade roughly triples your wealth.

This is why the single best financial decision you can make in your 20s is to start investing—even if it’s only $500/month. Time is the variable that can’t be recovered.

The Iron Law of Compounding: Start Early or Pay Later

Here’s a scenario that should terrify anyone in their 30s who hasn’t started investing yet.

Person A: Invests $6,000/year from age 25-35 (10 years), then stops. Never adds another dollar.

- Total invested: $60,000

- Balance at 65 (assuming 8%): $560,434

Person B: Invests $6,000/year from age 35-65 (30 years). Contributes 3x longer.

- Total invested: $180,000

- Balance at 65 (assuming 8%): $734,002

Person A invested $120,000 less and ends up with 76% of Person B’s wealth.

Now flip it:

Person C: Invests $6,000/year from age 25-65 (40 years). Never stops.

- Total invested: $240,000

- Balance at 65 (assuming 8%): $1,745,503

Person C has 2.4x more wealth than Person B despite only investing $60,000 more.

The lesson is brutal: You can’t make up for lost time by contributing more later. The math doesn’t work.

Starting at 25 vs. 35 is worth over $1 million in retirement wealth—even if you stop contributing after 10 years.

Why “Timing the Market” Is a Loser’s Game

Let’s address the elephant in the room.

Every year, someone gets the timing right. They sell before a crash. They buy at the bottom. They make 40-50% while everyone else is down.

Here’s why that doesn’t matter:

Studies show that missing just the 10 best days in the market over 30 years cuts your returns in half. And here’s the twist: 7 of the 10 best days typically happen within 2 weeks of the 10 worst days.

If you’re out of the market trying to “time the bottom,” you miss the recovery. And the recovery is where the money is made.

Real example: 2020 COVID crash

Market dropped 34% from Feb 19 to Mar 23, 2020.

If you panic-sold on March 23:

- You locked in a 34% loss

- You likely missed the 40% rebound from March 23 to June 8

- By the time you “felt safe” to re-enter, the market was already up 30%+

The disciplined investor who held through the crash:

- Stayed invested

- Maybe even deployed extra cash during the dip using a systematic DCA strategy

- Ended 2020 up 16%

The “smart” market timer:

- Sold at the bottom

- Waited for “confirmation”

- Re-entered too late

- Ended 2020 down 15-20%

The difference? Over $100,000 on a $500K portfolio.

Discipline beat timing. Like it always does.

The Hidden Costs That Destroy Compounding

Even if you understand the math, there are silent wealth killers that wreck your compound growth.

1. Fees

A 1% annual fee doesn’t sound like much. Over 30 years, it’s devastating.

Invest $500,000 at 8% for 30 years:

With 0.1% fees (index fund):

- Ending balance: $4,841,784

With 1% fees (actively managed fund):

- Ending balance: $3,927,571

You just paid $914,213 in fees.

That’s not a fee. That’s a second house you didn’t get to buy.

2. Taxes

Most people focus on returns. Smart people focus on after-tax returns.

If you’re in the 35% tax bracket and earn 8% in a taxable account:

- Your pre-tax return: 8%

- Your after-tax return: 5.2%

Over 30 years on $500,000:

8% pre-tax, taxable account:

- After taxes: $1,856,179

8% in a Roth IRA (tax-free growth):

- After taxes: $5,031,328

Tax-deferred accounts are worth $3.17 million more.

This is why maxing out your 401k, backdoor Roth, mega backdoor Roth, and HSA isn’t optional. It’s the difference between retiring comfortably and retiring wealthy.

3. Inflation

Your money needs to beat inflation, not just grow.

8% nominal returns with 3% inflation = 5% real returns.

Over 30 years, $500,000 at 5% real returns:

- Ending balance in today’s dollars: $2,160,664

Not bad. But if you assumed 8% without accounting for inflation, you thought you’d have $5,031,328 in purchasing power.

You’re off by $2.87 million in real wealth.

This is why you can’t just “save your way to wealth” in a savings account earning 4%. You’re barely keeping pace with inflation. You’re not getting ahead.

The Discipline Advantage: Why Boring Wins

Here’s what disciplined investors do that lucky investors don’t:

1. They automate everything.

- Auto-transfer $X to investment account every paycheck

- Auto-invest in index funds

- Auto-rebalance quarterly

- No decisions. No emotions. Just systems.

2. They ignore 95% of financial news.

Markets up? Cool. Markets down? Cool. Still investing the same amount every month.

3. They maximize tax-advantaged space first.

Before they invest a single dollar in taxable accounts, they max out:

- 401k: $23,500/year

- Backdoor Roth IRA: $7,000/year

- HSA: $4,300-$8,550/year

- Mega Backdoor Roth: Up to $46,000/year (if available)

That’s $40,000-$77,000/year in tax-advantaged contributions before touching taxable accounts.

4. They rebalance mechanically.

Once a year, they check their allocation. If stocks are up and bonds are down, they sell some stocks and buy bonds. Not because they’re “timing” anything. Because that’s the rule.

5. They never panic sell.

Markets drop 20%? They keep investing. Maybe even increase contributions slightly if they have cash on hand.

The boring, mechanical approach beats the “smart, active” approach 90% of the time over 30 years.

The Real Math: What Discipline Actually Looks Like in Numbers

Let me show you what disciplined wealth building looks like in practice.

Age 30:

- Starting balance: $50,000

- Monthly investment: $2,000 ($24,000/year)

- Strategy: 80% stock index funds, 20% bond index funds

- Rebalance: Annually

Age 40:

- Balance: ~$500,000

- Contributions: $240,000

- Growth: $260,000

Age 50:

- Balance: ~$1,400,000

- Contributions: $480,000

- Growth: $920,000

Age 60:

- Balance: ~$3,000,000

- Contributions: $720,000

- Growth: $2,280,000

Notice what happened:

- Your contributions were $720K

- Compound growth added $2.28 million

- Growth was 3x your contributions

That’s compounding. That’s discipline. That’s 30 years of boring, systematic investing.

No stock picks. No market timing. No crypto moonshots. Just:

- Contribute consistently

- Keep costs low

- Ignore noise

- Let time do the work

Why Lucky People Go Broke and Disciplined People Get Wealthy

I know people who made $500K in one year from crypto. Most of them are broke now.

I know people who never made more than $150K/year but retired with $4 million. They automated their investing in their 20s and never touched it.

The difference?

Lucky people:

- Make big wins

- Assume they’re smart

- Increase lifestyle to match wins

- Take bigger risks

- Eventually blow up

Disciplined people:

- Make boring gains

- Know it’s the system, not them

- Keep lifestyle stable

- Take measured risks

- Never blow up

Luck is fragile. Discipline is antifragile.

A lucky investor needs everything to go right. One bad bet, one market crash at the wrong time, one lifestyle inflation spiral—and they’re back to zero.

A disciplined investor can survive almost anything:

- Market crashes? Keep buying.

- Job loss? Have 6 months emergency fund.

- Inflation? Already invested in assets that grow.

- Taxes? Already maxed out tax-advantaged space.

The system protects them. Luck doesn’t protect anyone.

What This Means for You

If you’re in your 20s or 30s and you’re not investing yet, start today. Not next month. Today.

Even if it’s $200/month. Even if you feel like you should wait until you “have more saved.” You can’t buy time. Start small and increase as your income grows.

If you’re in your 40s and you haven’t been disciplined, it’s not too late, but you need to be more aggressive:

- Max out every tax-advantaged account

- Cut lifestyle inflation ruthlessly

- Invest 30-40% of gross income

- You’re making up for lost time, and it requires sacrifice

If you’re in your 50s and you’re behind, you need to combine:

- Maximum savings rate (40-50% of gross)

- Aggressive but not reckless asset allocation (70-80% stocks)

- Delay retirement by 3-5 years if needed

- Consider working part-time in “retirement” to let your portfolio compound

The math is unforgiving. But it’s also fair.

It doesn’t care about your story. It doesn’t care if you “didn’t know better” in your 20s. It just rewards those who deploy capital consistently over long periods.

The Bottom Line

Compounding rewards the disciplined. Not the lucky. Not the smart. Not the hardworking.

The disciplined.

If you can execute a boring plan—max out tax-advantaged accounts, invest in low-cost index funds, rebalance annually, ignore market noise—for 20-30 years, you will build wealth.

Not because you’re special. Because the math works.

A = P(1 + r)^t

Maximize P. Protect r. Extend t.

Everything else is noise.

Next in the series: Part 2: The 3 Engines of Wealth—Income, Investment, and Optionality

Action Items

If you take nothing else from this post, do these three things this week:

- Calculate your actual savings rate: Gross income – taxes – expenses = deployable capital. If it’s under 20%, you have a problem.

- Check if you’re maxing tax-advantaged space: Are you contributing the full $23,500 to your 401k? Have you done a backdoor Roth IRA this year? Are you using your HSA as an investment vehicle?

- Set up automation: Auto-transfer to investment account on payday. Auto-invest in index funds. Remove yourself from the decision loop.

The math doesn’t care about your intentions. It only cares about deployed capital and time.

Start today.

This is Part 1 of the Rational Compounding Framework. Read the complete framework to see how income, investment, and optionality work together.