Updated July 2026: HYSA rates have fallen further since this was written. The Fed has held at 3.50–3.75% through four consecutive 2026 meetings — no additional cuts materialized as expected. Top HYSA rates are now 3.80–4.10%, down from the 3.80–4.10% range discussed below. The CD ladder strategy remains the right call.

I noticed something when I was pulling together the Fed chair piece a couple of weeks ago. The post made a straightforward argument — Kevin Warsh wants to cut rates, the FOMC is divided but the direction is down, and the HYSA window that high earners have been enjoying since 2023 is narrowing. What I didn’t write was the follow-on question that piece implied: if rates are falling and HYSA yields are going with them, where does the cash that isn’t your emergency fund actually go?

The answer most financial advisors would give right now is some version of a CD ladder. That answer sounds boring. It is boring. It’s also the right one for a specific slice of your savings — and the mechanics of why it works in a falling-rate environment are slightly different from how most people explain it, so it’s worth walking through carefully.

What Changed and Why It Matters Right Now

The Federal Reserve cut its benchmark rate three times in late 2025 — September, October, December — and has held at 3.50–3.75% through every 2026 meeting so far. The effect on HYSA rates was nearly immediate with each cut. High-yield savings accounts adjust their rates within days of a Fed move, because they’re competing for deposits and their rate-setting is essentially market-driven in real time.

What Actually Happened to Rates — And Where They Sit Now

That’s the feature that makes HYSAs valuable — instant liquidity, no lock-in, rates that respond to the market. It’s also the feature that makes them less useful as a savings vehicle in a rate-falling environment. The 3.80–4.10% APYs that top competitive HYSAs are offering today are already materially lower than a year ago — and while the Fed has held at 3.50–3.75% through four 2026 meetings, additional cuts remain possible in late 2026. Every cut that lands translates to a lower HYSA yield within a few weeks.

A certificate of deposit does the opposite. When you lock in a CD today, the rate is fixed for the term you chose. A 12-month CD at 4.10% pays 4.10% for twelve months regardless of what the Fed does during that period. If the Fed cuts twice and HYSAs fall to 3.25% by next spring, the CD holder is still earning 4.10%. That rate protection is the entire case for CDs in a declining-rate environment — and it’s exactly the environment we’re in.

The complication is liquidity. A HYSA lets you move money whenever you need it. A CD charges an early withdrawal penalty — typically 90 days of interest for terms up to 12 months, 180 days of interest for longer terms — if you access the principal before maturity. Tie up your emergency fund in a CD and discover your car needs a new transmission in month three, and the penalty effectively reduces your yield significantly. This is why the structure of how you deploy money into CDs matters more than whether you use them at all.

The Emergency Fund Distinction Nobody Gets Right

Before the ladder mechanics, one line that should be non-negotiable: your emergency fund does not belong in a CD.

Three to six months of essential expenses — mortgage or rent, utilities, food, minimum debt payments, health insurance — should be in a HYSA with instant access and zero penalty for withdrawal. This money exists for emergencies, and emergencies don’t schedule themselves around your CD maturity dates. The entire value of an emergency fund is that you can access it within 24 hours without losing a chunk of the interest you’ve earned.

The money that belongs in a CD ladder is what sits beyond the emergency fund. It’s the excess cash you’ve accumulated above your liquidity buffer — a home down payment fund you won’t need for 18 months, a tax liability you’re holding for Q4, bonus income that landed and isn’t deployed yet, or simply savings you’ve built up that are earning HYSA rates not because you need them liquid but because you haven’t made a deliberate decision about them.

Join The Global Frame

Money, work, and tech — one read every Saturday that actually changes how you think.

Why CDs Outperform HYSAs in a Falling-Rate Environment

This distinction matters because a lot of CD ladder content lumps these together, creating the impression that you’re giving up liquidity you actually need. You’re not giving up liquidity on your emergency fund — that stays in the HYSA. You’re giving up flexibility on money that isn’t doing anything particularly useful by staying liquid, and trading that flexibility for a locked-in yield before rates fall further.

How a CD Ladder Actually Works

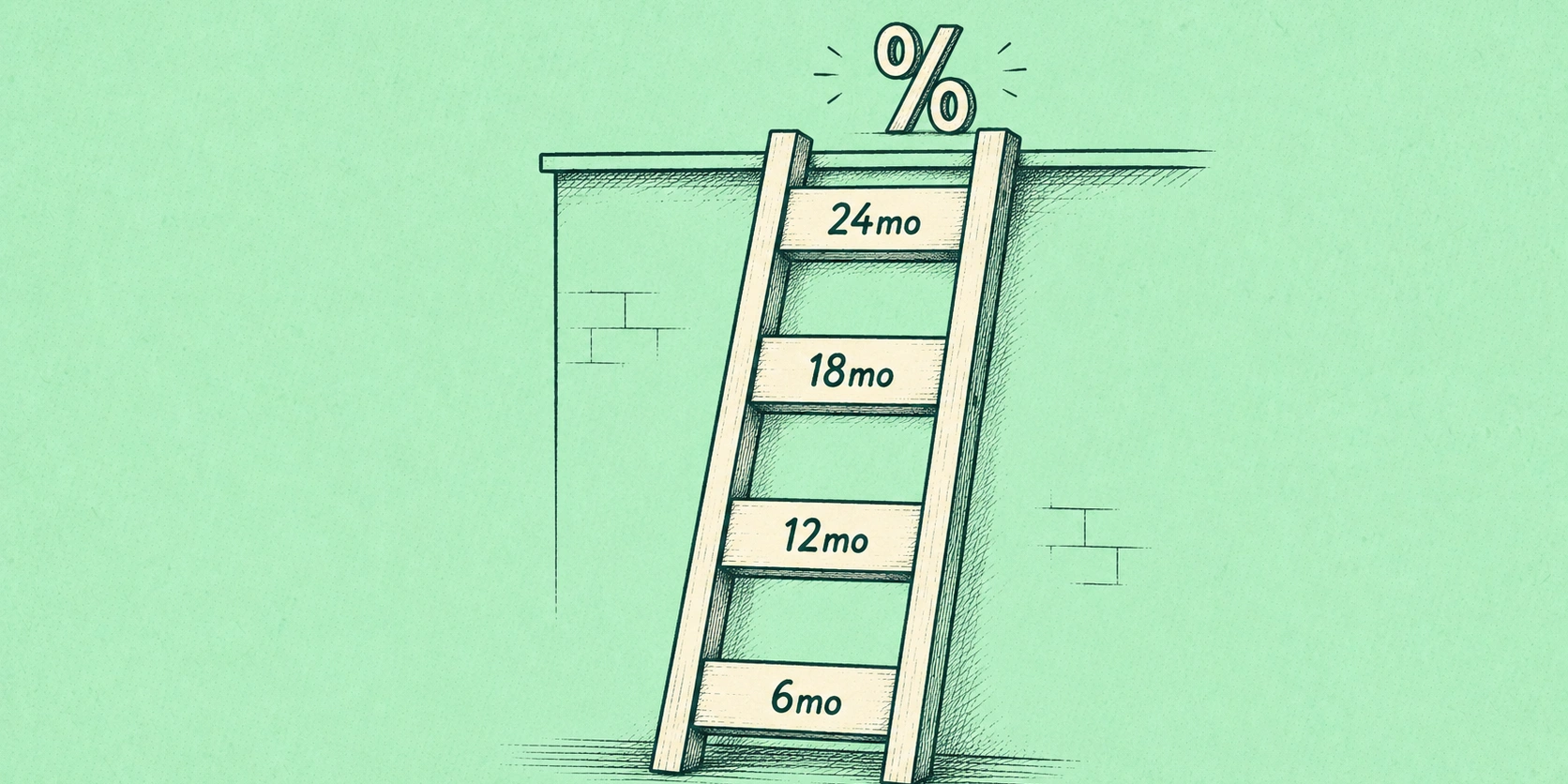

A CD ladder splits money across multiple CDs with staggered maturity dates so that a portion of your savings becomes available at regular intervals. Instead of putting $20,000 into a single 2-year CD and having no access to any of it for 24 months, you put $5,000 each into a 6-month, 12-month, 18-month, and 24-month CD. Every six months, one CD matures. You can take that cash if you need it, or roll it into a new CD at the longest term in your ladder.

The result is a savings structure that captures rates higher than a HYSA, protects some portion of your yield from Fed cuts, and provides rolling liquidity every six months rather than the complete illiquidity of a single long-term CD.

In the current rate environment, the specific numbers look like this. The best available rates as of this week, according to Bankrate’s May 25 survey: top 6-month CDs around 4.08–4.10% APY, top 12-month CDs around 4.10% APY, top 18-month CDs around 4.00% APY, top 24-month CDs around 4.05% APY. These are the rates at competitive online banks — not the national average, which sits at just 1.97% for 12-month CDs, meaning most people who have CDs at traditional banks are earning half the going market rate.

One important note: the April 2026 CPI came in at 3.8% annual inflation. A 4.10% CD rate beats inflation — but only barely, and only if you’re at a competitive institution. The case for CDs over HYSAs in this environment isn’t “CDs are great.” It’s “HYSAs are going to get worse faster than CDs will, and locking in 4.10% now is better than earning 3.25% on a HYSA a year from now.”

The Ladder to Build in 2026

A four-rung ladder using 6-month, 12-month, 18-month, and 24-month terms gives you access to a portion of your money every six months while capturing current rates across multiple terms. Here’s how it works with $20,000 in cash beyond your emergency fund — allocate $5,000 to each rung.

$5,000 in a 6-month CD at ~4.08% APY. This matures in roughly November 2026. At that point, if rates have fallen as expected, you roll it into a new 24-month CD — the longest rung in the ladder — capturing whatever rate is available at that time. If you need the cash, it’s there with no penalty.

How to Build a Simple Two-Rung Ladder Right Now

$5,000 in a 12-month CD at ~4.10% APY. Matures around May 2027. By then, Fed cuts may have brought HYSA rates meaningfully lower. You’re earning 4.10% through that period regardless.

$5,000 in an 18-month CD at ~4.00% APY. Matures around November 2027. Rolls or redeems.

$5,000 in a 24-month CD at ~4.05% APY. Matures around May 2028. The longest lock-in, but also the furthest protection against rate compression.

Over 24 months, this structure earns meaningfully more than leaving all $20,000 in a HYSA if rates fall by 75–100 basis points as current market expectations suggest. At 4.10% on a 12-month CD versus a HYSA that drifts from 4.25% to 3.50% over the same period, the difference on $20,000 is roughly $200–$350 annually — not life-changing, but it’s money that requires one afternoon of setup and zero ongoing effort.

The minimum deposits at competitive institutions are accessible: Limelight Bank requires $1,000, Marcus by Goldman Sachs requires $500, America First Credit Union requires $500. You don’t need $20,000 to start. A $4,000 ladder with $1,000 per rung captures the same rate protection at a fraction of the total.

The Early Withdrawal Penalty Math

The penalty structure deserves more attention than most CD explainers give it, because it determines how wrong you can afford to be about your liquidity needs before the CD strategy costs you money.

When a CD Ladder Makes Sense (And When It Doesn’t)

At Marcus by Goldman Sachs, the early withdrawal penalty on CDs up to 12 months is 90 days of interest. On a $5,000 CD at 4.05% for 12 months, total interest earned at maturity is $202. If you withdraw at month six — halfway through — you’d have earned $101 in interest, and the 90-day penalty is $50. You still net $51 in interest, a positive outcome, but one that’s lower than what a HYSA would have delivered with no penalty.

The scenarios where breaking a CD clearly costs you more than it saves: withdrawing in the first two months, when accrued interest is lower than the penalty amount; or breaking a longer-term CD (18 or 24 months) where penalties are 180 days of interest and the penalty can exceed interest earned if you exit early in the term.

The no-penalty CD addresses this risk directly. Ally Bank offers no-penalty CDs — officially an 11-month term — with no early withdrawal penalty after the first six days. The rate is lower than a standard CD by roughly 0.25–0.50%, but the ability to exit without cost makes them functionally a HYSA alternative that locks in a rate for 11 months. For the shortest rung of a ladder, or for money where you have genuine uncertainty about timing, a no-penalty CD is worth the rate concession.

The Account Setup That Matters Most

One practical detail that CD articles consistently undersell: the national average rate for a 12-month CD is currently 1.97%, per Bankrate’s May 25 data. The best available rate is 4.10%. That’s more than a 2-percentage-point spread between a mediocre choice and a good one — more than the entire benefit of building a ladder in the first place.

The single highest-leverage action in CD investing is not the ladder structure. It’s making sure you’re at a competitive institution rather than the bank that sent you a direct mail offer. The biggest traditional banks — Chase, Bank of America, Wells Fargo — routinely offer CD rates well below the market rate because they have the brand recognition and deposit base to attract customers without competing on yield. Online-only banks and credit unions compete directly on rate. The setup takes an afternoon: verify FDIC or NCUA insurance, confirm the rate and penalty terms in writing, fund the account via ACH transfer.

The HYSA yield cliff post I wrote at the start of the year argued that the 4%+ savings rate window was closing. That prediction has played out. The HYSA rates that were hitting 4.75–5.00% in mid-2024 have drifted down with each Fed cut since September. What the CD ladder does is give you a mechanism to lock in the rates that remain before they compress further.

The setup isn’t complicated. The ongoing management is minimal — a calendar reminder when each CD matures, and a decision about whether to roll or redeem. For money that isn’t your emergency fund and isn’t deployed in investments, it’s the most straightforward way to capture more yield than your HYSA will offer twelve months from now.

If you haven’t looked at your savings structure since the Fed started cutting, now is the window. Not because a dramatic move is required — the amounts involved don’t transform most financial lives. But because locking in 4.10% today rather than 3.25% next year on the same dollars, with the same level of risk, is the kind of marginal decision that compounds quietly and costs nothing to act on. The no-penalty CD is the liquid middle-ground worth understanding before you commit to a standard CD term, and switching to a higher-yield HYSA is step one if you’re still earning less than 3.80% on your savings.